A common stress we hear from advisors is the anxiety adult children in their 30s to 50s experience when talking to their parents about aging, future caregiving needs, and health changes. A significant concern in these conversations is the financial independence—or potential dependence—of their parents.

Will your clients outlive their retirement funds?

With retirement evolving significantly in recent decades, longevity has become a critical element of financial planning. With people living longer, continued inflation, and rising healthcare costs, outliving one’s retirement plan is a real concern.

This is why addressing health, longevity, and long-term care must be an integral part of every retirement planning session with senior clients. Here are some ways to initiate these important conversations.

1. Personalize Life Expectancy: The Foundation of a Solid Retirement Plan

No two clients are alike, so a one-size-fits-all approach won’t work for longevity planning. Many advisors use age 95 as a standard life expectancy in retirement projections because it’s conservative. However, more advisors are using longevity calculators to craft plans specific to each client’s health, lifestyle, and family history. This ensures that the plan reflects a more realistic life expectancy and avoids underestimating retirement needs.

When discussing longevity, consider asking questions like:

PRACTICE TIP: When considering whether to keep or surrender a life insurance asset, rely on independent experts who can value a life insurance policy based on the premiums and projected life expectancy. This process can uncover information that provides direction to planning.

2. Long-Term Care Projections: Why Longevity Matters

People are living longer—and that’s great news! But longer life spans can strain a financial plan that wasn’t designed to support decades of post-retirement living. Clients could face cash flow shortages in their later years without proper projections.

Consider a scenario where a client lives to 70 but requires long-term care in their final years. That client may spend more during retirement than a healthier individual who lives to 90 but doesn't need expensive care.

With nursing home costs averaging more than $100,000 a year, even partial reliance on Medicare and Medicaid may not be enough to cover long-term care expenses. This makes it vital to discuss health history, family health patterns, and potential longevity with your clients. It’s also essential to have open conversations about how they plan to fund care during their later years.

A conversation starter could be:

PRACTICE TIP: You can help take pressure off the adult children by helping their aging parents repurpose their life insurance and eliminate future premium obligations to pay for caregiving needs.

3. Longevity-Related Solutions: Funding Retirement and Long-Term Care

As the longevity economy grows, an increasing portion of the population will reach advanced age, potentially placing financial strain on younger family members. It’s crucial to explore various solutions for financing long-term care and late-stage retirement needs.

One option to consider is life settlements. A life settlement allows a policy owner to sell their life insurance policy for a lump sum of cash, often much higher than the cash surrender value. This transaction provides liquidity and eliminates future premium payments, freeing up funds for retirement, investments, or care needs.

Discussing this option with your clients might sound like:

PRACTICE TIP: Partner with an independent life settlement resource who has a fiduciary duty to your client and facilitates a secure policy auction that drives competition, guaranteeing the best offer.

In Conclusion

Conversations around longevity, health, and long-term care are essential for building comprehensive and realistic financial plans for your clients. By discussing these topics, you can help ensure your clients are financially prepared for a longer retirement and the potential care costs that come with it. Taking the time to understand each client’s unique circumstances will not only lead to better planning but also build trust and peace of mind for the future.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

The aftermath of COVID-19, the rise of AI tools, and new regulations are transforming how consumers engage with life insurance. Many of the largest wealth management and investment firms now offer independent consultative platforms for financial advisors and Registered Investment Advisors (RIAs) to partner with firms that specialize in services outside their wheelhouse—like longevity analysis and valuation of life insurance assets. It can be a valuable tool for planning firms aiming to thrive by providing comprehensive solutions. Whether preventing financial disaster or optimizing asset allocation for high-net-worth families, the life settlement market can be crucial in comprehensive financial planning and business growth.

Historically, uncertainty in financial markets increases life insurance lapse activity. Think about your parents and the large number of baby boomers who are retiring every day or already retired. What are they worried about?

According to the 2023 Transamerica Center for Retirement Studies Report, the most often cited retirement fears are declining health that requires long-term care (36%), Social Security will be reduced or cease to exist in the future (36%), outliving their savings and investments (35%), possible long-term care costs (30%), not being able to meet the financial needs of their family (30%), and cognitive decline, dementia, Alzheimer’s Disease (29%).

View the full article:

Schedule a 15-minute call to discuss how we help you integrate life settlements into your client conversations.

FAST TWITCH MUSCLES START TO ATROPHY BY THE AGE OF 30

By: Bill Clark | Senior Director

You can definitely engage in training exercises to slow the decline in fast twitch muscles, but there is a reason why most professional athletes retire in their 30s. My wife has been working out strenuously for more than forty years. She is 65 years old, and her VO2 max is in the upper 15% of women her age. Her physical strength allows her to be the active grandmother that everyone wishes they had for our ten grandchildren. To accomplish this, she has made it a habit to vary her exercise routines during the week. The other day, she went back to one of her old standbys, The Firm Aerobic Workout with Weights. She still uses her old Firm DVDs that were first created in 1986, but updated versions are readily available today: The Firm Workout & Exercise Videos | Gaia.

The Firm uses something called muscle confusion to make sure that all muscle groups are worked out over time. It all looks kind of hokey to me, but I must admit that I can’t even complete a session with her. Even my wife has begun to realize that she needs to modify her training regime if she wants to maintain balance and stability. One of the pieces of equipment they use in The Firm is a step-up box. You see a lot of step-up boxes being used in fitness clubs and CrossFit gyms. They are usually associated with men with big muscles using 100lb+ weights as they step onto a tall 24-inch box as they are preparing to be a Navy Seal or part of some Black Ops operation. At age 74, after breaking my back last year, I’m still struggling to do a proper step-up on a 10-inch step-up box with no weights, but I’m making progress. Oh, I could probably catapult myself up onto a 20-inch box, but I wouldn’t be using the right form to engage my fast twitch muscles, which I need for stability at my age.

These fast twitch muscles keep us from falling and breaking something as we age. They allow us to keep our balance if we slip on something or step off a curb without noticing the drop. They allow us to quickly apply the brakes to avoid a catastrophic fall. After the age of 70, if you fall and break your hip, it could be fatal or, at minimum, be a long, painful recovery period that reduces your quality of life. I’m reluctant to admit that I have had way too many falls on my mountain bike that have resulted in broken bones or serious soft tissue damage. I didn’t realize until now that many of those falls could have been avoided if I had spent more time developing my fast twitch muscles. My lack of stability provided by fast twitch muscles was readily apparent over the weekend when my 5-year-old grandson faked me out and blew past me for a touchdown during a backyard football game. You can bet that I’ve now made it a priority to fix that, and I will. I highly recommend this 30-second video, Defying Aging: Harnessing Eccentric Strength for a Life of Balance #shorts #peterattia (youtube.com), if you, your clients, or your parents are over the age of 60. The insights provided in this short video underscore the importance of seeking help to strengthen your fast twitch muscles. Also, if you are still in the prime of your working years, these insights could help ensure a longer and healthier life for you.

As I surfed the web last night, I found a good article in Men’s Health about developing fast twitch muscles: Your Guide to Fast-Twitch Muscle Training (menshealth.com). It reminded me that my wife laughed at me recently when I purchased yet another piece of fitness equipment, a jump rope. It turns out that it is a safe way to develop fast twitch muscles. The fact is, it will probably be hilarious when I first attempt to jump rope at my age. Wish me luck!

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

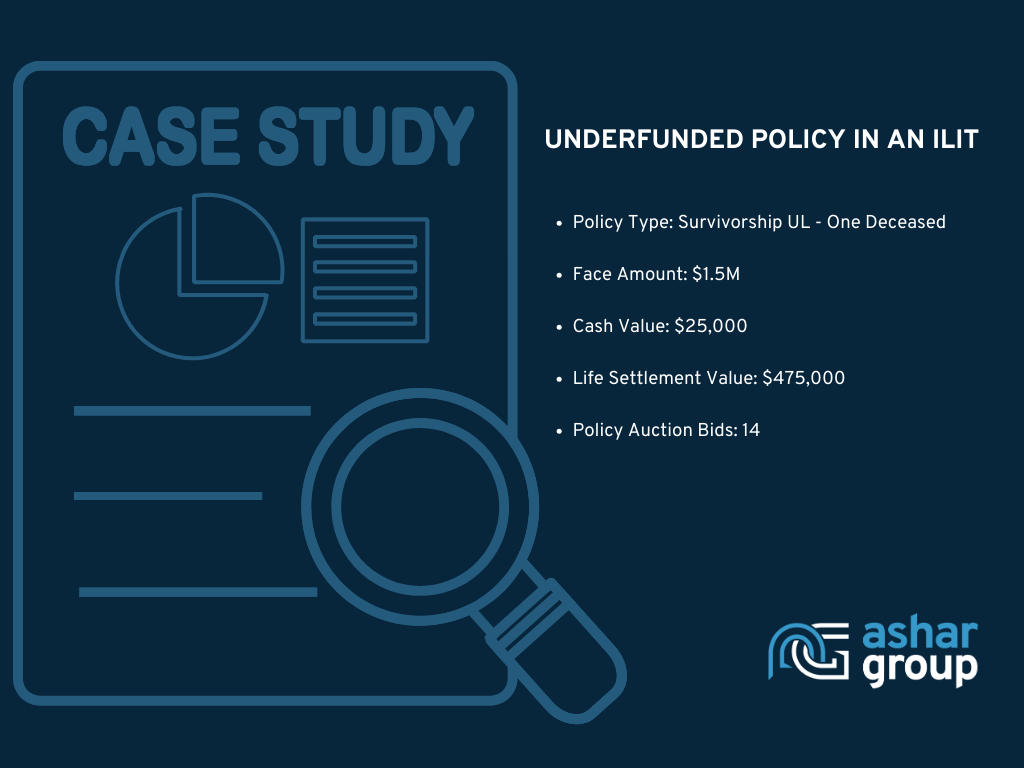

Considering the financial landscapes many clients are navigating, here's an everyday success story that underscores the importance of valuing assets, particularly life insurance, in crafting comprehensive planning solutions.

We recently worked with a client facing the challenge of an underfunded life insurance policy held within an Irrevocable Life Insurance Trust (ILIT). The policy, once thought to be a cornerstone of their estate plan, was underperforming and had become a source of financial strain due to rising premiums.

Challenges Faced:

Solution Implemented:

Results Achieved:

Impact on Comprehensive Planning: The funds from the life settlement were strategically reinvested, contributing to a more robust and diversified financial portfolio. This, in turn, allowed for the reevaluation and adjustment of the client's overall estate planning strategy.

This success story highlights the transformative impact of valuing and strategically managing life insurance assets within the context of comprehensive financial planning.

To find out if your client's policy may qualify for a life settlement, try our probability calculator.

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

In a recent conversation, an advisor shared the tension and anxiety related to adult children in their 30s to 50s having conversations with their parents about aging, future caregiving needs, and health changes. A key factor is financial independence or dependence on the family.

As retirement has changed over the past several decades, longevity has become a vital component of financial planning. With people living longer, continued inflation, and rising healthcare costs, outliving one’s retirement plan is a real concern.

This is why a frank discussion about health, longevity, and long-term care needs to be part of every retirement strategy session with your senior clients. Here are a few thoughts to get the conversation started with clients.

What type of information is discussed or gathered in ongoing planning discussions with clients? Many advisors use age 95 as a standard life expectancy for retirement planning because it’s a conservative estimate. When it comes to finances in one’s advanced years, being conservative is important. However, to develop the most sustainable financial plan, some advisors have opted to use a longevity calculator instead of the industry standard for every client. This will allow you to create a more personalized plan for every client.

Consider including the following question on planning checklists about physical and mental health, lifestyle, and their vision for what their life looks like in their late 80s to 90s.

"If there was a change to your health, where do you see yourself living? At home or in a community with others your age? Does this change if one spouse passes before the other?"

The good news can sometimes be the bad news. It's wonderful that people are living longer than anticipated, but often, their financial plan did not project them living into their late 80s to 90s. What if the planning is running low on cash flow? Retirement-age client’s health history and outlook are vital when it comes to effective retirement planning.

For example, a client who lives only to age 70 but spends the last five years of life in a long-term care facility could very well end up needing more money in retirement savings than a healthy person who ages in place and lives ten years longer.

Long-term care has become financially burdensome for most families, and those expenses continue to grow.

Since Medicare and Medicaid cover only a percentage of the care most people entering nursing facilities need, seniors - and their families - are left to make up the difference. With annual costs for a private room in a nursing home close to $110,000, that difference is often significant.

Having an open discussion of your client’s health history, family health history, and longevity expectations can help set realistic goals regarding how much they may need to cover long-term care.

"How are you planning to pay for those later years? The average cost can range between $5K- $10K per month for any higher quality option."

Over one-third of the country will be part of the longevity economy, which in turn could financially impact the remaining two-thirds of the country. How are families prepared to address the potential cash requirements for their aging parents and loved ones? This is also a good time to bring an alternative for paying for long-term care – life settlements. This solution allows clients to sell their life insurance policy for a lump sum of cash that’s greater than the policy’s cash surrender value.

On average, a life settlement transaction using a competitive auction platform through an independent life settlement broker can earn your client 5x the cash surrender value. This not only creates liquidity but also eliminates future premium obligations, allowing those funds to be used for other planning needs like retirement, investments, and long-term care.

"Do you foresee your adult children or someone else assisting in paying for long-term care? Have you explored all available options to fund these needs?"

Longevity Throws a Wild Card in Even the Best-Laid Plans

Society of Financial Service Professionals

by Jamie L. Mendelsohn, EVP, Ashar Group

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

Enjoy more blogs in our Longevity Series:

Shooting for the Centenarian Club

The Keys to Longevity – It’s Never Too Late but Start Now!

By: Bill Clark | Senior Director, Ashar Group

Longevity Series - Blog #2 (2-minute read)

Experts agree that VO2 max and muscular strength are the keys to longevity. It’s never too late to get started, but the benefits can be greater if you start the right training program during your prime working years. The more I study the secrets of longevity, the more confused I become. I’ve come to realize that you have to look for common themes and then try something to see if it works for you. I’m age 74 and trying to turn back the clock physiologically and end up living longer and healthier. I’ve always been involved in athletic endeavors, but I realize now that what I have been doing is not enough.

For the time being, I’m an enthusiastic fan of Peter Attia, a medical doctor who wrote the book OUTLIVE- The Science and Art of Longevity. Some of his material is very in-depth, and there are some YouTube spots that are very short and informative. It’s not a bad place to start your journey to live longer and healthier by listening to this short conversation, VO₂ Max and Muscular Strength: The Keys to Longevity, from the Tim Ferris show. You could bury yourself in YouTube videos and podcasts by Peter Attia and other “experts” on longevity.

For me, this whole journey is going to take me longer than I thought, but it’s worth it. I just started this Longevity Insights blog series, and I’m not even sure where I’m going with it yet, so you’ll have to be patient with me. I know that my main objective is to help people at all stages in life find information that will make their lives better and more fulfilling. It’s meant to apply to people of all ages and physical abilities and to financial professionals, their clients, and centers of influence. My next post will be on “Why we fall as we age”. If you are age 50 or older, you better “step up” right now (no pun intended, as you will see in the next blog). If you are younger, it pays huge dividends to incorporate the right training into your schedule now. The key to living a long and healthy life starts when we are too busy working and raising a family to give it the attention it deserves. The cost may be too high for you to ignore it. Stay tuned.

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

A corporate-owned life insurance policy is generally purchased to protect a business in the event a key partner/employee of that business passes away. Among other benefits, the insurance policy helps to bridge the gaps the death of that individual causes and ensures the company continues to function. But what happens to that policy with the individual retires?

Life insurance may have considerable value that can be uncovered by an independent appraisal. Like any other asset – real estate, jewelry, automobiles, artwork – value depends on what the market will bear. Life insurance value on the secondary market can vary depending on the conditions present at the time of sale. To avoid your business clients making uninformed decisions, paying unnecessary premium payments, or missing lucrative planning opportunities, it is important to understand the fair market value of a corporate-owned policy first.

The primary factors in determining the value of a life insurance policy are the policy details and the estimated life expectancy of the insured.

Policy details include:

Life expectancy is estimated based on:

When selecting an appraiser to value the life insurance policy, it’s important to choose an independent resource – one that does not have any interest in purchasing the policy but who also has the knowledge, qualifications, and historical comps to provide an accurate analysis that allows your clients to make an informed decision and ensures their best interests are served.

There are many planning scenarios where a life insurance valuation would benefit your clients. One reason is that the appraisal may uncover significant life settlement value. In some cases, exchanging the policy for cash now makes the most sense. In the case of this retiring business owner, the life settlement was more than the value of the business itself.

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

Advisors ask their compliance departments, “How can I tell my clients that I provide comprehensive and holistic financial planning yet not disclose the life settlement option when appropriate?” With an aging population, many clients prefer to receive a buyout of their existing life insurance for an amount that is higher than their cash surrender value, providing liquidity for investments and other retirement needs.

View the full article:

Longevity Series - Blog #1 (4-minute read)

This is personal. If you’re not paying attention to clients like me, you’re missing out on a huge growing segment of the financial planning arena driven by baby boomers. At my age (74), I’m on the leading edge of the boomers.

In September of last year, I broke my back when took a Superman flight over the handlebars of my mountain bike. I knew immediately this was different than my previous accidents where I was sidelined for several weeks because of torn muscles and ligaments in my shoulders. This time, I couldn’t walk for a while and my thumb and two fingers on my right hand were numb. This one really scared me.

This kind of accident can easily take you out of the game if you’re over age 70. Over the next several weeks, I lost significant muscle mass in my legs. I started physical therapy and sold my mountain bike and bought a recumbent trike with a motor assist so that I could stay active and keep up with my wife on paved trails. Until recently, I found it impossible to get up off the floor without assistance. I’m fortunate to be married to a health nut that still rocks her mountain bike at age 65. I was healthy before the accident and determined to get even healthier now with her help and the example she sets. Peter Attia, author of the New York Times #1 Best Seller “Outlive” is now one of my health mentors. His video is a real eye opener. Be sure to click on the pdf link below the video. This morning, my Garmin watch told me that my fitness age is now down to 71.5 years and my VO-2 max is increasing. I’m shooting for a fitness age of 67 within the next year.

I work in the life settlement market where 87% of settled policies are on insureds age 70-100+ (Source: Ashar Group). Clearly, this is a market that gives the advantage to retirement age clients. Many of these insureds have shortened life expectancies due to health issues or increased longevity. Health arbitrage is a key factor influencing the value of a policy in the settlement market. I own a 20-year convertible term policy that is reaching the end of its term shortly. You can bet on the fact that I’m going to check to see if it has any value on the secondary market before my term period ends. Secretly, I hope that it doesn’t have any value because my life expectancy will be too long. God willing, I hope to be a centenarian in good health and enjoying life to its fullest.

The focus of my financial planning has now switched to maintaining a healthy and active lifestyle until the angels come calling. Joseph F. Coughlin, founder of the MIT AgeLab and author of the #1 New York Times bestseller The Longevity Economy, provides the insight business leaders and financial planners need to serve the growing older market: a vast, diverse group of consumers representing every possible level of health and wealth, worth about $8 trillion in the United States alone and climbing.

BTW, I recently purchased an all-road bike and got back on two wheels, but not on mountain bike trails. It works a whole new set of leg muscles, and nine months after my accident I was able to get off the floor this morning using only my legs. I thought I might never see that again. Pay heed to the financial needs of “boomers” who are bound and determined to live longer and stay healthy and active. Because of increasing longevity, they need to reset their financial planning horizon with your help. Gotta go now. Amazon just delivered a new piece of fitness equipment to my doorstep.

Bill joined Ashar Group in 2006. He has been instrumental in helping financial professionals understand longevity planning to better serve their clients.

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.