Does your life insurance policy still serve its original purpose?

Policy owners put life insurance in place for many reasons. Over time, the policy may no longer serve its original purpose, or the premiums become unaffordable, and it is time to consider alternative options. A life settlement can be the solution to funding long-term care, covering medical costs, or retirement needs.

Unlike applying for insurance coverage, no medical exam is required in the life settlement process. Buyers will review the last 3 years of medical records for the purpose of providing offers. Certain situations do not require any medical review at all.

The right to sell your life insurance policy, like any other piece of property/asset, is available in all 50 states.

With the retirement crisis and increased medical costs, more senior policy owners are using life settlements to unlock the value of unwanted/unneeded life insurance policies and use the funds for all sorts of needs like funding retirement, long-term care, or medical expenses.

Companies on TV are licensed to represent investors, not policy owners. Their objective is to pay the lowest amount possible for a policy without competition. Ashar is a fiduciary to the policy owner and through our competitive auction process, we secure hundreds of millions each year for families looking to solve everyday needs. Since 2003, Ashar has been focused solely on the life settlement and life insurance policy valuation space and has earned the reputation of a trusted resource.

While we’re licensed to represent the seller in a life settlement transaction, Ashar also works alongside financial professionals for the clients they serve. We believe policy owners are best served when their planning professionals are involved in any complex decisions about their life insurance. Either way, our sole fiduciary duty is to you – the policy owner. Ashar has relationships with thousands of reputable financial professionals in every practice area – insurance planning, tax planning, retirement planning, wealth management, charitable planning, etc. If you need a recommendation, let us make the connection. We’re here to help.

It depends on several factors like cost of insurance changes or significant changes in insured’s health. Like all markets, sometimes it’s a seller’s market and sometimes it’s a buyer’s market. Also, the market is impacted by buyer’s purchase parameters. Ultimately, families should consider the cost of continued premiums and managing the policy should they decide to keep it in the hopes of selling it in the future. What if the insured lives longer than projected? Does the policy owner have the liquidity available to maintain the policy?

Most buyers are looking at policy type, age and health of the insured, and premium requirements to make a determination of offer. Each life settlement buyer is a fiduciary to multiple investors, each with their own unique set of purchase parameters. Based on policy details and insured health status, we will reach out to our extensive network of institutional buyer relationships for offers. If you have an unneeded/unwanted policy, are ages 60s to 90s, and have had a decline in health since your policy was issued, you could qualify for a life settlement solution. Younger insureds with significant health issues can also qualify.

The overall value depends on several factors: policy type, premium amount, cash surrender value, insured’s health, and buyer’s purchase parameters. Most policy owners only know what the death benefit is in the event of the insured’s passing. Beyond that, some policies accumulate cash value – the amount the policy owner would receive if the policy were surrendered (less any carrier/outstanding fees). In the life settlement transaction, there are two values: the offer that is received without a policy auction and the fair market value (highest value) – achieved only through a true policy auction. Find out if your policy could have value.

Ashar can provide a range of potential value with some policy and medical information within a day or two. The entire process takes on average about the same amount of time as selling your house. Ashar’s experienced team is dedicated to compressing timeframes and delivering a quick result to every policy owner and financial professional we serve.

Experienced life settlement resources work with qualified licensed purchasers. These purchasers are obligated to the investors they represent and are comprised of some of the most well-known institutional investment groups – pension plans, private equity, and asset managers. Ashar requires each buyer relationship to complete a due diligence process. We never work with purchasers who represent individual investors, or those that do not abide by all applicable regulatory requirements.

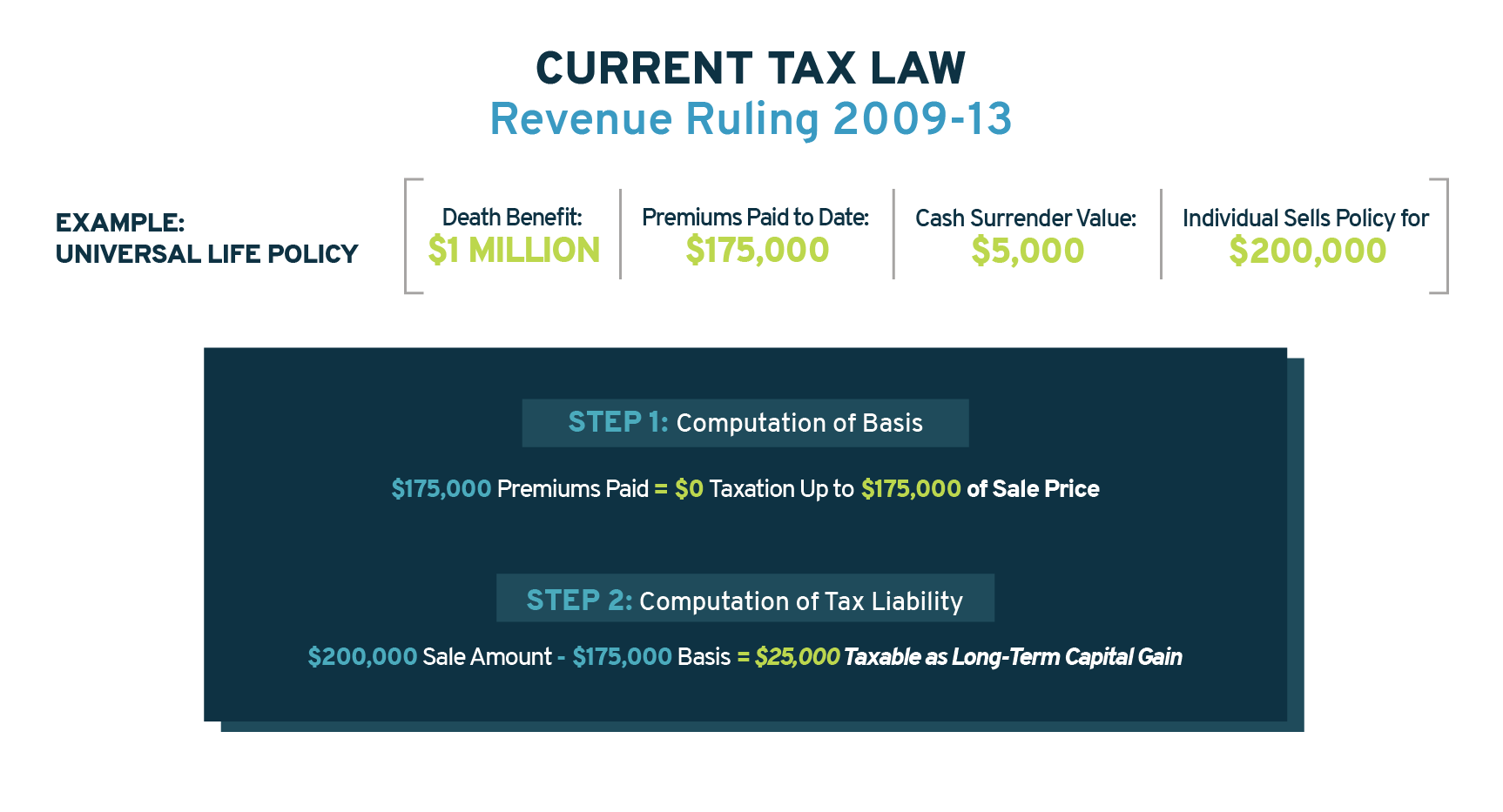

Money received from a life settlement is tax free up to the basis (premiums paid into the policy). From the basis to the cash surrender value is treated as ordinary income. All proceeds that exceed the cash surrender value is taxed as capital gain. *Disclaimer: This information is for educational purposes only. Ashar does not provide tax advice. Please speak with your tax professional for more information.