1. DETERMINE IF THE POLICY IS NEEDED

Valuing existing life insurance assets is a crucial step in preparing clients for changes that could impact their financial plans. Life insurance is a protection tool and a vital asset in wealth transfer strategies, retirement planning, and estate management. Upcoming tax policy revisions may alter the need to maintain the coverage. By assessing the current value of these policies, advisors can help clients make informed decisions about whether to keep, sell, or change existing policies.

Practice Tip: Examine your clients' existing life insurance portfolios for life settlement opportunities. Don't allow clients to lapse or surrender unneeded life insurance policies without first checking for life settlement value. It could result in a capital event that funds other planning.

2. KNOW WHAT TO LOOK FOR

IDEAL CLIENT

LOOK FOR CLIENTS IN FINANCIAL TRANSITION

3. PROTECT YOUR CLIENT'S BEST INTERESTS WITH A COMPLIANCE-CENTRIC LIFE SETTLEMENT RESOURCE

PRACTICE TIP: Ask these questions to make sure a life settlement resource is 100% aligned with you and your client.

Learn more about the state of the market from one of the nation's leading experts on life insurance valuation and life settlements.

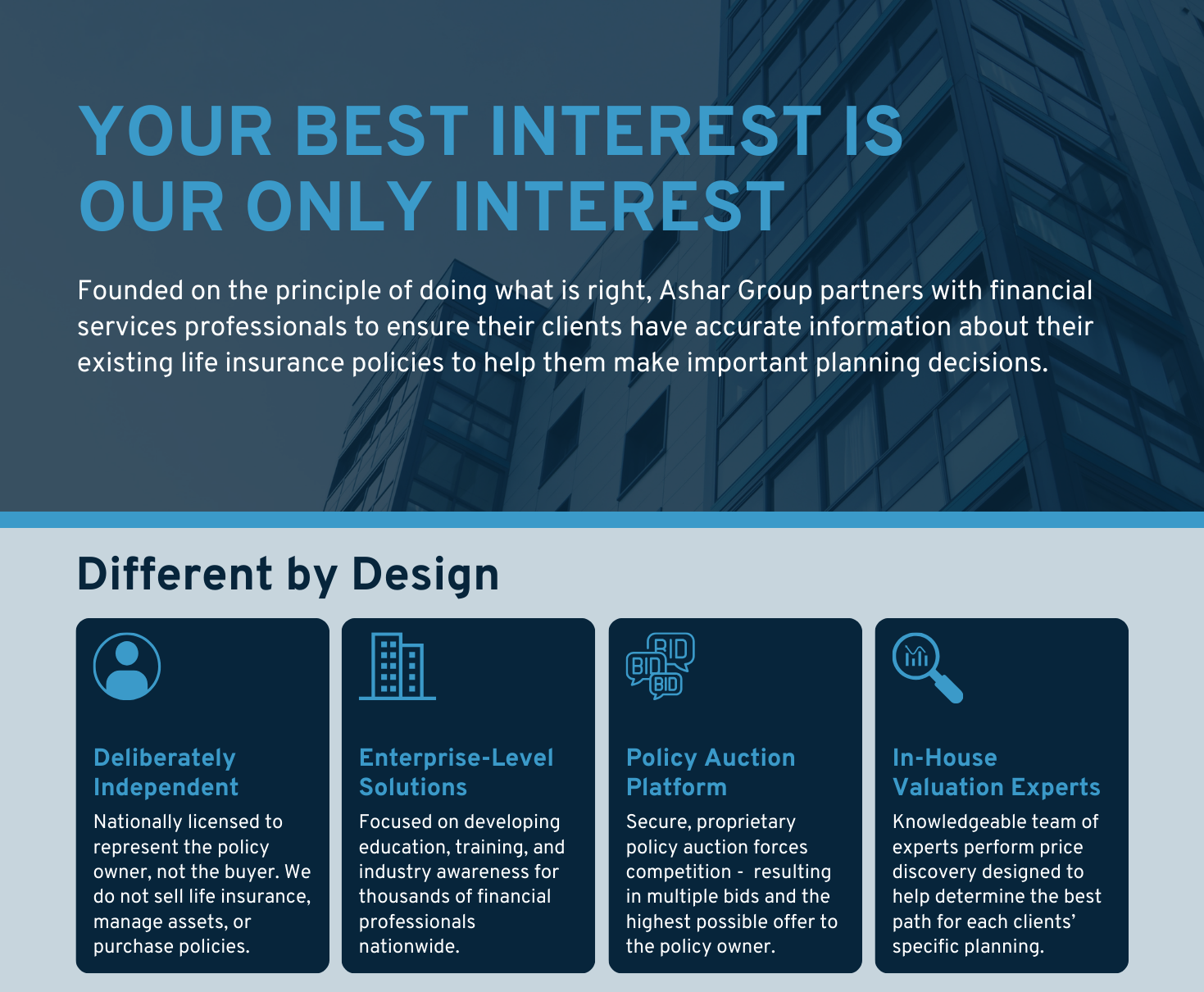

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

Business was sold, and the policy was no longer needed

Business owner was able to receive additional value above and beyond the sale of the company.

Their needs had changed, and they no longer needed the policy

They were able to uncover significant liquidity and fund their retirement.

Financial ripple effect caused reductions in cash flow

Used the cash to fund their livelihood.

Policy was underfunded and sitting in an ILIT

Eliminated future premium payments and used the funds for medical bills.

Liquidity constraints reduced donations

Cash created donation for the charity she loves.

Surrendering policy and interested in receiving more money

Adult children unable to pay premiums to maintain the policy.