For some charities, life insurance is a taboo subject, and they often surrender donated policies without any analysis. With approximately 51% of the U.S. population owning life insurance, it’s too large an asset class to omit from charitable planning discussions with donors, particularly considering the tremendous opportunities.

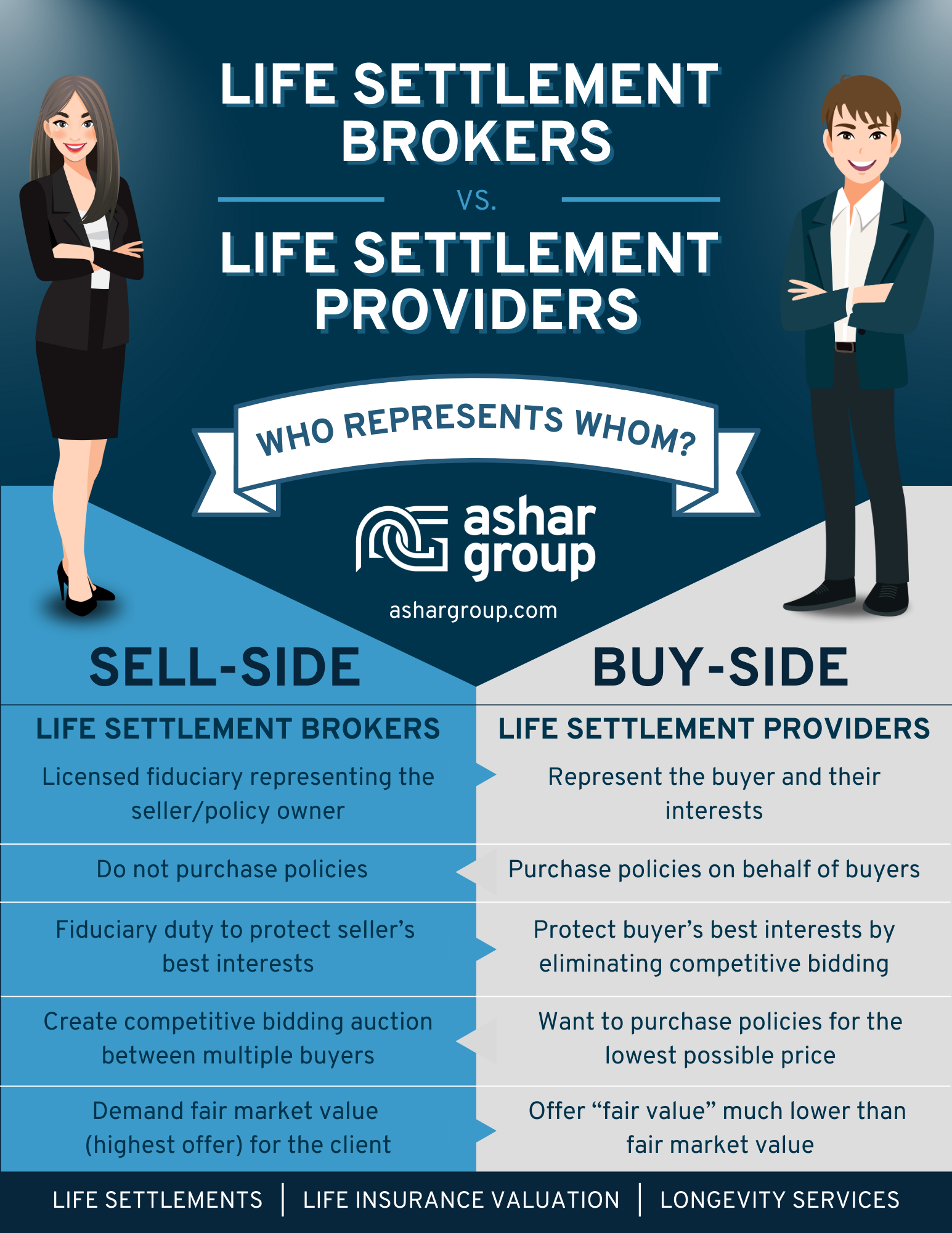

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients, specializing in life insurance valuation for planning purposes.

...And the youngest of them turn 61 this year.

As the financial landscape continues to evolve, so too must the approach of today's financial advisor. Gone are the days when retirement planning stopped at age 85. With more clients living into their 90s and beyond, comprehensive planning must now stretch across longer time horizons. The means anticipating new risks, uncovering new opportunities, and using tools like life settlements to help clients maximize their long-term financial security.

Advancements in healthcare, improved lifestyles, and greater awareness of wellness have all contributed to a significant rise in life expectancy. According to a recent article, many clients - especially those in higher-income brackets - have a very real chance of living into their 90s or even longer. This longevity shift can strain retirement income projections and long-term care strategies if not properly considered.

Advisors can no longer plan to age 85. Retirement strategies must now account for 30 to 40-year retirements, demanding smarter planning, more flexible assets, and more nuanced conversations with clients.

Living longer is a gift - but it comes with a price tag. Increased healthcare costs, long-term care, inflation, and the risk of outliving assets are very real concerns for retirees. Clients fear becoming a financial burden to their families or having to sacrifice quality of life late in retirement.

It's crucial for advisors to start the longevity conversation early. Educating clients about the financial realities of extended lifespans can help them make more informed, proactive decisions. It's also a natural segue into evaluating underutilized assets that could support their long-term needs, such as life insurance policies.

An often overlooked but powerful tool in the longevity toolkit is a life settlement - the sale of an unwanted or unneeded life insurance policy for a lump sum that exceeds the cash surrender value (and is less than the death benefit). For clients in their 70s, 80s, and even 90s, this can be a strategic move that unlocks hidden value in a policy that no longer fits their goals.

Consider a client who took out a large policy to protect a growing family or business, but now finds those needs have changed. Instead of lapsing the policy or surrendering it for minimal value, a life settlement can provide immediate funds that support long-term care needs, retirement lifestyle, or estate planning goals.

Clients are often unaware of the option (or are duped by direct-to-consumer advertising), and their advisors are in the best position to educate them. When integrated into a comprehensive plan, life settlements can:

Advisors who ignore the longevity risk are not just missing a piece of the puzzle, they are missing a core component of modern financial planning. By acknowledging longer lifespans and incorporating strategies like life settlements, advisors can offer peace of mind and financial confidence that lasts a lifetime - and beyond.

As the industry continues to shift, advisors will stand out not just for managing assets, but for managing expectations and delivering solutions that evolve as life gets longer.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

In a nutshell, your client can have some serious health issues that disqualify them for new insurance, but still have a relatively long life and therefore not qualify for a life settlement. It's because insurance carriers are underwriting different risk factors at policy issue compared to institutional buyers who purchase existing life insurance policies.

Life insurance carriers are concerned about mortality risk - the risk of the insured passing too soon. Their underwriting places emphasis on health and lifestyle debits to determine life expectancy. They look at the worst-case scenario.

Insitutional life settlement buyers are concerned about longevity risk - the risk of the insured living too long. Their underwriting looks at the debits, but also health and lifestyle credits. They focus on the best-case scenario.

There are 2 main factors institutional buyers consider when determining whether the purchase of an existing life insurance policy is a good investment:

It's all about the math. In some cases, high premiums can kill a life settlement deal for an insured with health issues that would lead to a decline for new insurance. For example, if the policy has an 8%-10% premium ratio (annual premium/face value), then the life expectancy of the insured would have to be shorter for it to be attractive to buyers. Conversely, a policy with a low premium ratio (1%-3%) allows for a longer life expectancy and is still considered a good investment for buyers.

The best way to ensure your client gets the most for their unneeded/unwanted life insurance policies in a life settlement is to execute an auction that forces buyer competition. Buyers are looking for the best rate of return for the investors they represent. Just like with real estate, when buyers compete, the client (and the advisor) win!

Ashar Group is a nationally licensed independent seller’s representative. We sit on the same side of the table as the planning professional and their client, ensuring the policy owner’s best interests are protected. Because we don’t purchase the policies, our sole responsibility is to the client. Through our auction platform, we create competition between buyers to ensure policy owners are getting the best offer.

PRACTICE TIP: Ask these three questions of your life settlement resource to ensure your client has independent representation in the life settlement transaction:

Learn more about the difference between sell-side and buy-side.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

June, an 84-year-old widow, saw something in a television ad that piqued her interest. After husband Frank passed away two years ago from a long battle with heart disease, June found herself in an assisted living facility, burdened by mounting medical bills. While knitting a baby blanket for her new great-granddaughter one afternoon, a captivating commercial flickered across her TV screen, promising relief from her financial worries. It touted the option of selling her life insurance policy for cash through something called a life settlement. Intrigued, she set aside her knitting and jotted down the contact information.

Why did June consider a life settlement? As June pondered the possibility, she realized she no longer had a pressing need for the policy. Her children were grown and financially stable, yet she was still shelling out hefty premiums to maintain coverage. "Why not explore this further?" she thought. With a simple phone call to the number from the commercial, June received a cash offer of $75,000 in less than 48 hours. The offer was three times greater than the $25,000 cash surrender value of her policy.

The offer seemed almost too good to be true, stirring both excitement and unease within June. She felt pressured to make a quick decision and was unfamiliar with the company pushing the deal. Was she being targeted by another financial scam aimed at unsuspecting seniors?

Seeking clarity, June turned to her trusted advisor, Michael, who assured her it wasn't a scam but urged caution. He explained that many direct-to-consumer marketers aim to purchase policies at a steep discount, prioritizing their interests over the sellers'. Instead, Michael suggested consulting a life settlement broker with a fiduciary duty to secure the best deal for June.

Michael contacted Ashar Group, a reputable firm specializing in appraising life insurance assets and facilitating life settlements. With Michael's guidance and Ashar Group's expertise, June embarked on a journey to maximize the value of her policy. Together, they compiled compelling information to present through the policy auction, where multiple buyers would compete for the opportunity to purchase her policy. Just like in a real estate bidding war, this competitive environment drove up the value of June's policy.

Though the process took longer than the initial 48 hours, June felt no pressure to rush, and the outcome was beyond her wildest expectations. The auction yielded 14 separate bids, with the winning offer coming in at a staggering 19 times higher than the cash surrender value. What's more, the winning bid came from the very same buyer who had initially offered her only three times the cash surrender value. The key to this remarkable outcome? The competition created by the auction process, coupled with thorough underwriting, uncovered the true value of June's policy.

The moral of the story is clear: Seniors should exercise caution when tempted by direct-to-consumer life settlement ads on TV and social media. Instead, entrust their interests to a nationally licensed life settlement broker like Ashar Group, ensuring they receive the best possible outcome.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

A common stress we hear from advisors is the anxiety adult children in their 30s to 50s experience when talking to their parents about aging, future caregiving needs, and health changes. A significant concern in these conversations is the financial independence—or potential dependence—of their parents.

Will your clients outlive their retirement funds?

With retirement evolving significantly in recent decades, longevity has become a critical element of financial planning. With people living longer, continued inflation, and rising healthcare costs, outliving one’s retirement plan is a real concern.

This is why addressing health, longevity, and long-term care must be an integral part of every retirement planning session with senior clients. Here are some ways to initiate these important conversations.

1. Personalize Life Expectancy: The Foundation of a Solid Retirement Plan

No two clients are alike, so a one-size-fits-all approach won’t work for longevity planning. Many advisors use age 95 as a standard life expectancy in retirement projections because it’s conservative. However, more advisors are using longevity calculators to craft plans specific to each client’s health, lifestyle, and family history. This ensures that the plan reflects a more realistic life expectancy and avoids underestimating retirement needs.

When discussing longevity, consider asking questions like:

PRACTICE TIP: When considering whether to keep or surrender a life insurance asset, rely on independent experts who can value a life insurance policy based on the premiums and projected life expectancy. This process can uncover information that provides direction to planning.

2. Long-Term Care Projections: Why Longevity Matters

People are living longer—and that’s great news! But longer life spans can strain a financial plan that wasn’t designed to support decades of post-retirement living. Clients could face cash flow shortages in their later years without proper projections.

Consider a scenario where a client lives to 70 but requires long-term care in their final years. That client may spend more during retirement than a healthier individual who lives to 90 but doesn't need expensive care.

With nursing home costs averaging more than $100,000 a year, even partial reliance on Medicare and Medicaid may not be enough to cover long-term care expenses. This makes it vital to discuss health history, family health patterns, and potential longevity with your clients. It’s also essential to have open conversations about how they plan to fund care during their later years.

A conversation starter could be:

PRACTICE TIP: You can help take pressure off the adult children by helping their aging parents repurpose their life insurance and eliminate future premium obligations to pay for caregiving needs.

3. Longevity-Related Solutions: Funding Retirement and Long-Term Care

As the longevity economy grows, an increasing portion of the population will reach advanced age, potentially placing financial strain on younger family members. It’s crucial to explore various solutions for financing long-term care and late-stage retirement needs.

One option to consider is life settlements. A life settlement allows a policy owner to sell their life insurance policy for a lump sum of cash, often much higher than the cash surrender value. This transaction provides liquidity and eliminates future premium payments, freeing up funds for retirement, investments, or care needs.

Discussing this option with your clients might sound like:

PRACTICE TIP: Partner with an independent life settlement resource who has a fiduciary duty to your client and facilitates a secure policy auction that drives competition, guaranteeing the best offer.

In Conclusion

Conversations around longevity, health, and long-term care are essential for building comprehensive and realistic financial plans for your clients. By discussing these topics, you can help ensure your clients are financially prepared for a longer retirement and the potential care costs that come with it. Taking the time to understand each client’s unique circumstances will not only lead to better planning but also build trust and peace of mind for the future.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

Historically, uncertainty in financial markets increases life insurance lapse activity. Think about your parents and the large number of baby boomers who are retiring every day or already retired. What are they worried about?

According to the 2023 Transamerica Center for Retirement Studies Report, the most often cited retirement fears are declining health that requires long-term care (36%), Social Security will be reduced or cease to exist in the future (36%), outliving their savings and investments (35%), possible long-term care costs (30%), not being able to meet the financial needs of their family (30%), and cognitive decline, dementia, Alzheimer’s Disease (29%).

View the full article:

Schedule a 15-minute call to discuss how we help you integrate life settlements into your client conversations.

FAST TWITCH MUSCLES START TO ATROPHY BY THE AGE OF 30

By: Bill Clark | Senior Director

You can definitely engage in training exercises to slow the decline in fast twitch muscles, but there is a reason why most professional athletes retire in their 30s. My wife has been working out strenuously for more than forty years. She is 65 years old, and her VO2 max is in the upper 15% of women her age. Her physical strength allows her to be the active grandmother that everyone wishes they had for our ten grandchildren. To accomplish this, she has made it a habit to vary her exercise routines during the week. The other day, she went back to one of her old standbys, The Firm Aerobic Workout with Weights. She still uses her old Firm DVDs that were first created in 1986, but updated versions are readily available today: The Firm Workout & Exercise Videos | Gaia.

The Firm uses something called muscle confusion to make sure that all muscle groups are worked out over time. It all looks kind of hokey to me, but I must admit that I can’t even complete a session with her. Even my wife has begun to realize that she needs to modify her training regime if she wants to maintain balance and stability. One of the pieces of equipment they use in The Firm is a step-up box. You see a lot of step-up boxes being used in fitness clubs and CrossFit gyms. They are usually associated with men with big muscles using 100lb+ weights as they step onto a tall 24-inch box as they are preparing to be a Navy Seal or part of some Black Ops operation. At age 74, after breaking my back last year, I’m still struggling to do a proper step-up on a 10-inch step-up box with no weights, but I’m making progress. Oh, I could probably catapult myself up onto a 20-inch box, but I wouldn’t be using the right form to engage my fast twitch muscles, which I need for stability at my age.

These fast twitch muscles keep us from falling and breaking something as we age. They allow us to keep our balance if we slip on something or step off a curb without noticing the drop. They allow us to quickly apply the brakes to avoid a catastrophic fall. After the age of 70, if you fall and break your hip, it could be fatal or, at minimum, be a long, painful recovery period that reduces your quality of life. I’m reluctant to admit that I have had way too many falls on my mountain bike that have resulted in broken bones or serious soft tissue damage. I didn’t realize until now that many of those falls could have been avoided if I had spent more time developing my fast twitch muscles. My lack of stability provided by fast twitch muscles was readily apparent over the weekend when my 5-year-old grandson faked me out and blew past me for a touchdown during a backyard football game. You can bet that I’ve now made it a priority to fix that, and I will. I highly recommend this 30-second video, Defying Aging: Harnessing Eccentric Strength for a Life of Balance #shorts #peterattia (youtube.com), if you, your clients, or your parents are over the age of 60. The insights provided in this short video underscore the importance of seeking help to strengthen your fast twitch muscles. Also, if you are still in the prime of your working years, these insights could help ensure a longer and healthier life for you.

As I surfed the web last night, I found a good article in Men’s Health about developing fast twitch muscles: Your Guide to Fast-Twitch Muscle Training (menshealth.com). It reminded me that my wife laughed at me recently when I purchased yet another piece of fitness equipment, a jump rope. It turns out that it is a safe way to develop fast twitch muscles. The fact is, it will probably be hilarious when I first attempt to jump rope at my age. Wish me luck!

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

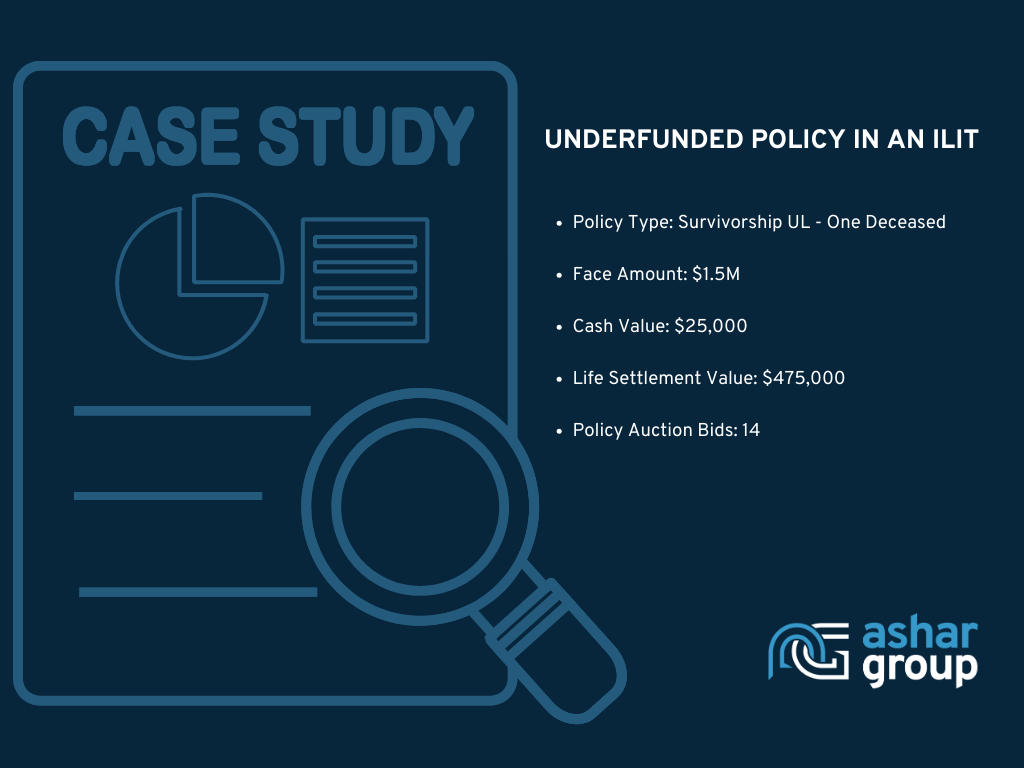

Considering the financial landscapes many clients are navigating, here's an everyday success story that underscores the importance of valuing assets, particularly life insurance, in crafting comprehensive planning solutions.

We recently worked with a client facing the challenge of an underfunded life insurance policy held within an Irrevocable Life Insurance Trust (ILIT). The policy, once thought to be a cornerstone of their estate plan, was underperforming and had become a source of financial strain due to rising premiums.

Challenges Faced:

Solution Implemented:

Results Achieved:

Impact on Comprehensive Planning: The funds from the life settlement were strategically reinvested, contributing to a more robust and diversified financial portfolio. This, in turn, allowed for the reevaluation and adjustment of the client's overall estate planning strategy.

This success story highlights the transformative impact of valuing and strategically managing life insurance assets within the context of comprehensive financial planning.

To find out if your client's policy may qualify for a life settlement, try our probability calculator.

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

In a recent conversation, an advisor shared the tension and anxiety related to adult children in their 30s to 50s having conversations with their parents about aging, future caregiving needs, and health changes. A key factor is financial independence or dependence on the family.

As retirement has changed over the past several decades, longevity has become a vital component of financial planning. With people living longer, continued inflation, and rising healthcare costs, outliving one’s retirement plan is a real concern.

This is why a frank discussion about health, longevity, and long-term care needs to be part of every retirement strategy session with your senior clients. Here are a few thoughts to get the conversation started with clients.

What type of information is discussed or gathered in ongoing planning discussions with clients? Many advisors use age 95 as a standard life expectancy for retirement planning because it’s a conservative estimate. When it comes to finances in one’s advanced years, being conservative is important. However, to develop the most sustainable financial plan, some advisors have opted to use a longevity calculator instead of the industry standard for every client. This will allow you to create a more personalized plan for every client.

Consider including the following question on planning checklists about physical and mental health, lifestyle, and their vision for what their life looks like in their late 80s to 90s.

"If there was a change to your health, where do you see yourself living? At home or in a community with others your age? Does this change if one spouse passes before the other?"

The good news can sometimes be the bad news. It's wonderful that people are living longer than anticipated, but often, their financial plan did not project them living into their late 80s to 90s. What if the planning is running low on cash flow? Retirement-age client’s health history and outlook are vital when it comes to effective retirement planning.

For example, a client who lives only to age 70 but spends the last five years of life in a long-term care facility could very well end up needing more money in retirement savings than a healthy person who ages in place and lives ten years longer.

Long-term care has become financially burdensome for most families, and those expenses continue to grow.

Since Medicare and Medicaid cover only a percentage of the care most people entering nursing facilities need, seniors - and their families - are left to make up the difference. With annual costs for a private room in a nursing home close to $110,000, that difference is often significant.

Having an open discussion of your client’s health history, family health history, and longevity expectations can help set realistic goals regarding how much they may need to cover long-term care.

"How are you planning to pay for those later years? The average cost can range between $5K- $10K per month for any higher quality option."

Over one-third of the country will be part of the longevity economy, which in turn could financially impact the remaining two-thirds of the country. How are families prepared to address the potential cash requirements for their aging parents and loved ones? This is also a good time to bring an alternative for paying for long-term care – life settlements. This solution allows clients to sell their life insurance policy for a lump sum of cash that’s greater than the policy’s cash surrender value.

On average, a life settlement transaction using a competitive auction platform through an independent life settlement broker can earn your client 5x the cash surrender value. This not only creates liquidity but also eliminates future premium obligations, allowing those funds to be used for other planning needs like retirement, investments, and long-term care.

"Do you foresee your adult children or someone else assisting in paying for long-term care? Have you explored all available options to fund these needs?"

Longevity Throws a Wild Card in Even the Best-Laid Plans

Society of Financial Service Professionals

by Jamie L. Mendelsohn, EVP, Ashar Group

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

Enjoy more blogs in our Longevity Series:

Shooting for the Centenarian Club

The Keys to Longevity – It’s Never Too Late but Start Now!

Broker-dealers, banks, ILIT trustees, insurance carriers, and planners with a fiduciary duty understand that part of protecting clients' best interests means offering all the available options and recommendations to help clients meet their planning goals. When it comes to life insurance, many factors affect whether a policy still meets the original purchase goal. As policy owners age, they outlive their original planning goals, interest rates affect policy performance, and life situations change. Therefore, the need for their life insurance coverage may change too. Sometimes that means exiting a life insurance policy that no longer serves a positive financial purpose.

There is a valuable alternative to lapse or surrender. A life settlement is a buyout of an existing life insurance policy for more than the cash surrender value and less than the death benefit.

Over time, compliance officers have come to recognize that if life settlements are pursued for the right reasons, after a thorough review of all non-forfeiture options and suitability, a life settlement could very well be in clients' best interests. It is a viable exit strategy that should be disclosed in a comprehensive policy review in partnership with a resource that offers a compliance-centric process. However, broker-dealers do not just allow life settlements carte blanche. They put strict procedural guardrails in place to protect the company and their representatives from liability risk.

When you or your client encounter marketing by a life settlement company, they may all sound the same. It is exceedingly difficult for even the most experienced advisors to differentiate between a company representing their client's best interests and one representing the buyers. There are multiple factors compliance officers consider when selecting a life settlement company. However, there are common mistakes to avoid that revolve around ensuring that your clients receive independent and knowledgeable representation that protects their best interests.

Ensuring the life settlement company has a fiduciary duty to your client, the policy owner, is the most critical factor in approving a compliance-centric resource.

There are key elements that compliance officers look for when completing their due diligence in the approval of a life settlement partner.

Although compliance officers are responsible for protecting the best interests of the company they represent, they have historically hesitated to approve life settlements for advisors to offer as an option to clients. Ninety percent of states regulate settlements, alleviating past concerns and helping to integrate this solution into mainstream planning. Broker-dealers do not advertise or promote life settlements, so we encourage advisors to check with their compliance department to ask if they have an approved life settlement resource.

Over the past 20 years, we have undergone numerous lengthy due-diligence processes and assisted in designing compliance-centric workflows for many of the largest nationally recognized broker-dealers. Discover how we're different by design.

Ashar Group is a nationally licensed life settlement firm that acts as a fiduciary to protect the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

{kind=link}