As a financial advisor who works with older clients, you’re likely familiar with elder financial abuse. Perhaps you’ve even helped a client through a financially abusive experience.

As a financial advisor who works with older clients, you’re likely familiar with elder financial abuse. Perhaps you’ve even helped a client through a financially abusive experience.

Whether or not you’ve seen this issue firsthand, you may be surprised to know just how rampant a problem it is. (more…)

So much of our adult lives is spent working to acquire money. We want to increase our income, improve our investment returns, add to our retirement accounts.

So much of our adult lives is spent working to acquire money. We want to increase our income, improve our investment returns, add to our retirement accounts.

Once we’ve sent our children through college, reached our retirement funding goals, and accomplished what’s important to us, those of us who want to can shift to a new way of thinking. We can start deciding how we’re going to give our money away. (more…)

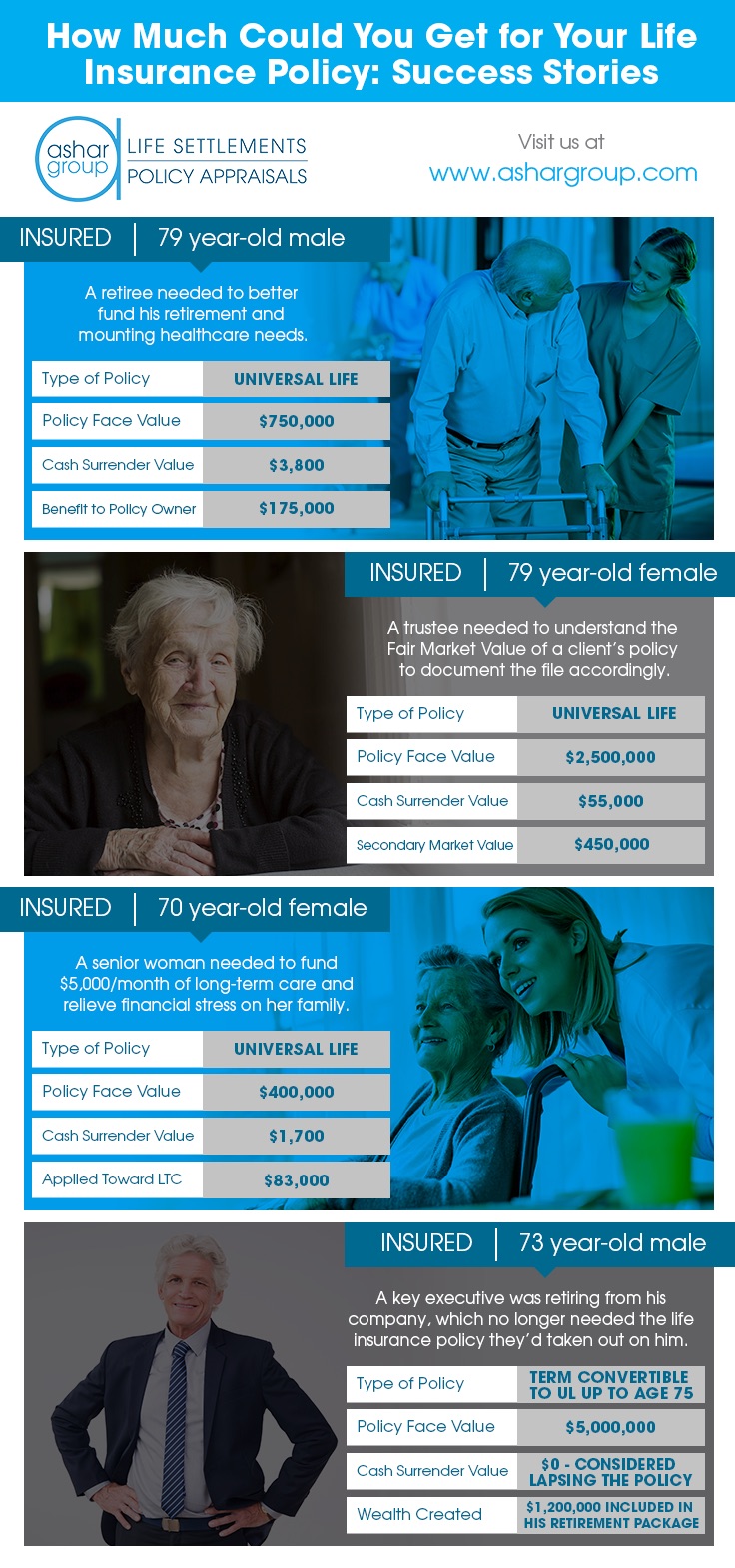

If you’re a financial planner who works with retirement-age clients, the topic of life settlements should be a regular part of planning conversations.

If you’re a financial planner who works with retirement-age clients, the topic of life settlements should be a regular part of planning conversations.

Life settlements allow a life insurance policyholder to sell their policy to an institutional buyer for more than the policy's cash surrender value, but less than the net death benefit. The purchaser of the policy assumes responsibility for all future premium payments and receives the death benefit when the insured passes away. (more…)

If you or a loved one has had to enter a hospital in the last several years, you’re undoubtedly familiar with this scene that was recently highlighted by the AARP.

If you or a loved one has had to enter a hospital in the last several years, you’re undoubtedly familiar with this scene that was recently highlighted by the AARP.

The patient is lying in a hospital bed, either awaiting or recovering from a procedure. Suddenly, a staff person who isn’t a doctor or nurse enters the room and introduces themselves as a member of the billing team. They talk to the patient and any family members present about what the bill is expected to cost, and ask how they would like to pay it. (more…)

Sooner or later, given enough time, most elderly adults will require care assistance, with much of this assistance requiring long-term care. While 65% of those needing care rely exclusively on those close to them, another 30% will employ paid providers for supplemental assistance.

Sooner or later, given enough time, most elderly adults will require care assistance, with much of this assistance requiring long-term care. While 65% of those needing care rely exclusively on those close to them, another 30% will employ paid providers for supplemental assistance.

In contrast to men, women are significantly overrepresented as care providers and provide the majority of support in a complex system of long-term care. According to an article published by the National Center on Caregiving, Women and Caregiving: Facts and Figures, the informal care provided by women to aging parents, spouses, friends, neighbors, and so forth ranges from $148 billion to $188 billion annually.

We all know that a positive outlook can have an immense effect on your quality of life. If you’re looking for silver linings, you’ll generally find them - if all you look for are clouds, that’s what you’ll see.

We all know that a positive outlook can have an immense effect on your quality of life. If you’re looking for silver linings, you’ll generally find them - if all you look for are clouds, that’s what you’ll see.

This can become even more important during retirement. Seniors who work hard to maintain a positive outlook during this major life change can reap real, concrete benefits. (more…)

Contemporary Alzheimer’s disease treatment has long been dominated by drug-based interventions. Though pharmaceutical approaches have shown some success in halting cognitive decline, their use is quite limited and not without the many serious side effects that may accompany the use of any drug. (more…)

Contemporary Alzheimer’s disease treatment has long been dominated by drug-based interventions. Though pharmaceutical approaches have shown some success in halting cognitive decline, their use is quite limited and not without the many serious side effects that may accompany the use of any drug. (more…)

As many families know all too well, Alzheimer’s is a devastating disease in so many ways.

As many families know all too well, Alzheimer’s is a devastating disease in so many ways.

According to the Alzheimer’s Association, in 2016, 5.5 million Americans had this illness, and 15 million Americans provided unpaid care for someone with the disease. That means Alzheimer’s is affecting at least 20.5 million Americans in a highly personal, day-to-day basis. (more…)