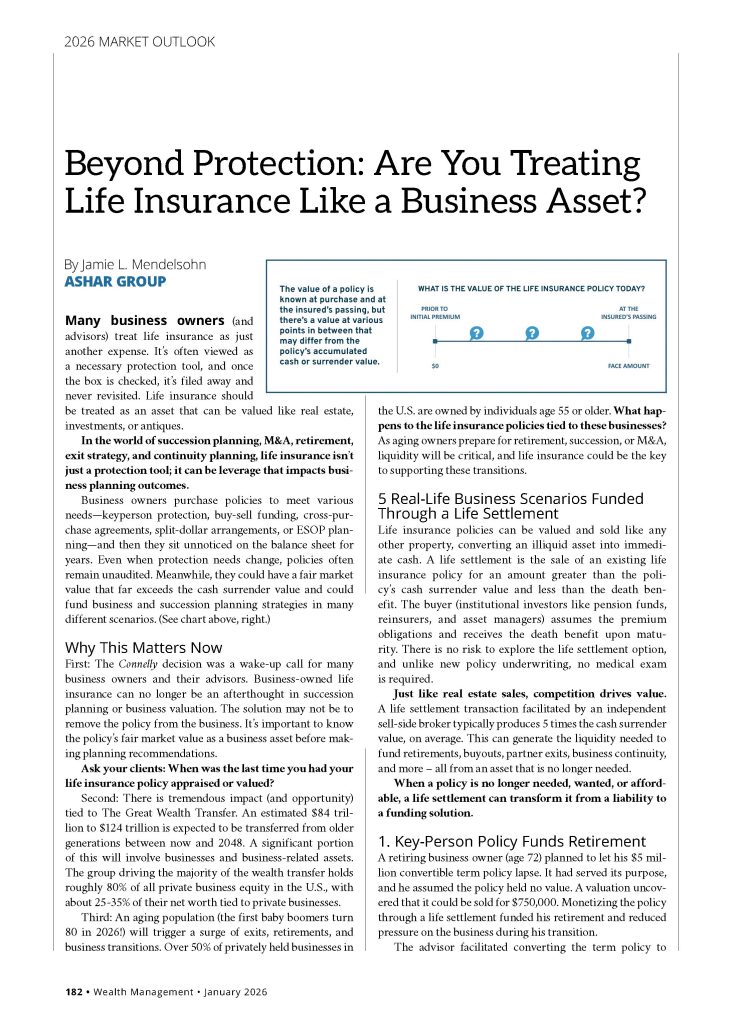

Many business owners (and advisors) treat life insurance as just another expense. It’s often viewed as a necessary protection tool, and once the box is checked, it’s filed away and never revisited. Life insurance should be treated as an asset that can be valued like real estate, investments, or antiques. In the world of succession planning, M&A, retirement, exit strategy, and continuity planning, life insurance isn’t just a protection tool; it can be leverage that impacts business planning outcomes.

Ashar Group is a nationally licensed sell-side life settlement firm that protects policy owners’ best interests by facilitating a competitive policy auction to deliver the best value to sellers. We are an independent resource for fiduciary advisors and their clients, specializing in life insurance valuation for planning purposes. Ashar Group does not sell life insurance, manage assets, or purchase policies.

For some charities, life insurance is a taboo subject, and they often surrender donated policies without any analysis. With approximately 51% of the U.S. population owning life insurance, it’s too large an asset class to omit from charitable planning discussions with donors, particularly considering the tremendous opportunities.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients, specializing in life insurance valuation for planning purposes.

What would you do if you could free up $600,000 a year and unlock $5 million in hidden value without selling a single traditional asset? That was the question facing a family office managing the estate of an 85-year-old patriarch who had spent a lifetime building a family legacy...

Read the full Wealth Management 2025 Midyear Outlook

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients, specializing in life insurance valuation for planning purposes.

By Jamie L. Mendelsohn | EVP | Ashar Group

Article published in 2025 Wealth Management Market Outlook

By evaluating clients’ existing policies, advisors can uncover opportunities to convert underperforming or unneeded life insurance into liquid assets through the life settlement solution that can be reinvested to align with clients’ broader financial goals.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients, specializing in life insurance valuation for planning purposes.

Likely, you discuss real estate, trusts, businesses, retirement funds, and other equities with your clients at length. But what about their life insurance policy?

A life settlement is the sale of an existing life insurance policy to an institutional investor for more than the cash surrender value and less than the death benefit. The funds from a life settlement can be used for other planning needs - investments, new insurance on healthier insureds, retirement, charitable donations, and much more.

SUCCESS STORIES

We value thousands of policies each year. View more more life settlement success stories here.

Not every life insurance policy will qualify, but the ones that do can be sold for much more than their cash surrender value.

Try our Life Settlement Probability Calculator to determine if your client's policy could qualify.

Many financial professionals feel they don’t know enough about life insurance or life settlements to discuss this solution with their clients. We're here to help answer your questions about the market and guide you and your client through the process.

Complete the form below and a member of our Strategic Partnerships team will reach out to schedule a time for your life settlement market update with one of our experts.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

Trust & Estates Article - April 2024 | Jon B. Mendelsohn, CEO

You may be faced with a client who asks you for advice about selling their insurance policy. Before you can help your clients evaluate whether a life settlement is right for them, you should understand the three stages of the life settlement process.

More than 9M policies lapse each year, and only about 3,000 life settlement transactions occur. How many more of those lapsed policies could have qualified for a life settlement – a buyout of existing life insurance for an amount greater than the cash surrender value and less than the death benefit?

If only 1% of those lapsed could have qualified, that’s 90,000 policies resulting in billions to consumers over the cash surrender value.

From paying for long-term care and retirement planning to increased AUM, your clients can benefit from exchanging unwanted/unneeded/affordable life insurance policies for cash – recouping past premiums paid and eliminating future premium burdens.

As a trusted advisor, you're undoubtedly aware of the financial strain that can arise when life insurance policies no longer align with your client's needs. The cost of waiting can be significant, both in terms of diminishing cash values and escalating premium obligations.

These resources are designed to empower you as a trusted advisor to provide timely and strategic solutions for clients facing dwindling cash values and increased premium burdens.

Early Detection: Encourage clients to assess their life insurance policies early before they consider lapse/surrender, especially if they are experiencing cash value reductions or struggling with rising premiums. Timely evaluations enable you to identify potential life settlement opportunities before the situation worsens.

TOOL #1: Request the Planning Checklist for Existing Life Insurance – this will help you ask the right questions about your client’s existing life insurance policies.

Education and Awareness: Educate clients about the option of life settlements and make them aware of the potential financial benefits. Many policyholders are not fully informed about the possibilities available to them, and your guidance can be instrumental in helping them make informed decisions.

TOOL #2 : Request an in-person or virtual for your team(s) from one of our executive team members.

Collaboration with a Fiduciary to the Policy Owner: Partner with an independent life settlement seller’s representative who employs a policy auction that creates competition and increases the offers to policy owners. Engaging with experienced professionals can help expedite evaluations, negotiations, and the overall settlement process.

TOOL #3: NAEPC Journal Article – Maximizing Life Settlement Value Through a Policy Auction

Strategic/Comprehensive Planning: Incorporate life settlement considerations into your client's overall financial planning strategies. By proactively addressing the changing dynamics of their life insurance policies, you contribute to more resilient and adaptive financial plans.

TOOL #4: Life Settlement Probability Calculator – determine the likelihood that the policy has value in order to start the conversation.

Regular Policy Reviews: Conduct regular reviews of your client's life insurance policies to stay ahead of any shifts in their financial landscape. This proactive approach allows you to identify life settlement opportunities as soon as they arise.

TOOL #5: Contact us to help you navigate this process.

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

By: Bill Clark | Senior Director, Ashar Group

Longevity Series - Blog #2 (2-minute read)

Experts agree that VO2 max and muscular strength are the keys to longevity. It’s never too late to get started, but the benefits can be greater if you start the right training program during your prime working years. The more I study the secrets of longevity, the more confused I become. I’ve come to realize that you have to look for common themes and then try something to see if it works for you. I’m age 74 and trying to turn back the clock physiologically and end up living longer and healthier. I’ve always been involved in athletic endeavors, but I realize now that what I have been doing is not enough.

For the time being, I’m an enthusiastic fan of Peter Attia, a medical doctor who wrote the book OUTLIVE- The Science and Art of Longevity. Some of his material is very in-depth, and there are some YouTube spots that are very short and informative. It’s not a bad place to start your journey to live longer and healthier by listening to this short conversation, VO₂ Max and Muscular Strength: The Keys to Longevity, from the Tim Ferris show. You could bury yourself in YouTube videos and podcasts by Peter Attia and other “experts” on longevity.

For me, this whole journey is going to take me longer than I thought, but it’s worth it. I just started this Longevity Insights blog series, and I’m not even sure where I’m going with it yet, so you’ll have to be patient with me. I know that my main objective is to help people at all stages in life find information that will make their lives better and more fulfilling. It’s meant to apply to people of all ages and physical abilities and to financial professionals, their clients, and centers of influence. My next post will be on “Why we fall as we age”. If you are age 50 or older, you better “step up” right now (no pun intended, as you will see in the next blog). If you are younger, it pays huge dividends to incorporate the right training into your schedule now. The key to living a long and healthy life starts when we are too busy working and raising a family to give it the attention it deserves. The cost may be too high for you to ignore it. Stay tuned.

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

Advisors ask their compliance departments, “How can I tell my clients that I provide comprehensive and holistic financial planning yet not disclose the life settlement option when appropriate?” With an aging population, many clients prefer to receive a buyout of their existing life insurance for an amount that is higher than their cash surrender value, providing liquidity for investments and other retirement needs.

View the full article:

Business was sold, and the policy was no longer needed

Business owner was able to receive additional value above and beyond the sale of the company.

Their needs had changed, and they no longer needed the policy

They were able to uncover significant liquidity and fund their retirement.

Restaurant owner in his early 70s

Businesses were severely affected by the COVID-19 pandemic.

Longevity Series - Blog #1 (4-minute read)

This is personal. If you’re not paying attention to clients like me, you’re missing out on a huge growing segment of the financial planning arena driven by baby boomers. At my age (74), I’m on the leading edge of the boomers.

In September of last year, I broke my back when took a Superman flight over the handlebars of my mountain bike. I knew immediately this was different than my previous accidents where I was sidelined for several weeks because of torn muscles and ligaments in my shoulders. This time, I couldn’t walk for a while and my thumb and two fingers on my right hand were numb. This one really scared me.

This kind of accident can easily take you out of the game if you’re over age 70. Over the next several weeks, I lost significant muscle mass in my legs. I started physical therapy and sold my mountain bike and bought a recumbent trike with a motor assist so that I could stay active and keep up with my wife on paved trails. Until recently, I found it impossible to get up off the floor without assistance. I’m fortunate to be married to a health nut that still rocks her mountain bike at age 65. I was healthy before the accident and determined to get even healthier now with her help and the example she sets. Peter Attia, author of the New York Times #1 Best Seller “Outlive” is now one of my health mentors. His video is a real eye opener. Be sure to click on the pdf link below the video. This morning, my Garmin watch told me that my fitness age is now down to 71.5 years and my VO-2 max is increasing. I’m shooting for a fitness age of 67 within the next year.

I work in the life settlement market where 87% of settled policies are on insureds age 70-100+ (Source: Ashar Group). Clearly, this is a market that gives the advantage to retirement age clients. Many of these insureds have shortened life expectancies due to health issues or increased longevity. Health arbitrage is a key factor influencing the value of a policy in the settlement market. I own a 20-year convertible term policy that is reaching the end of its term shortly. You can bet on the fact that I’m going to check to see if it has any value on the secondary market before my term period ends. Secretly, I hope that it doesn’t have any value because my life expectancy will be too long. God willing, I hope to be a centenarian in good health and enjoying life to its fullest.

The focus of my financial planning has now switched to maintaining a healthy and active lifestyle until the angels come calling. Joseph F. Coughlin, founder of the MIT AgeLab and author of the #1 New York Times bestseller The Longevity Economy, provides the insight business leaders and financial planners need to serve the growing older market: a vast, diverse group of consumers representing every possible level of health and wealth, worth about $8 trillion in the United States alone and climbing.

BTW, I recently purchased an all-road bike and got back on two wheels, but not on mountain bike trails. It works a whole new set of leg muscles, and nine months after my accident I was able to get off the floor this morning using only my legs. I thought I might never see that again. Pay heed to the financial needs of “boomers” who are bound and determined to live longer and stay healthy and active. Because of increasing longevity, they need to reset their financial planning horizon with your help. Gotta go now. Amazon just delivered a new piece of fitness equipment to my doorstep.

Bill joined Ashar Group in 2006. He has been instrumental in helping financial professionals understand longevity planning to better serve their clients.

Ashar Group is a nationally licensed life settlement firm representing the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.