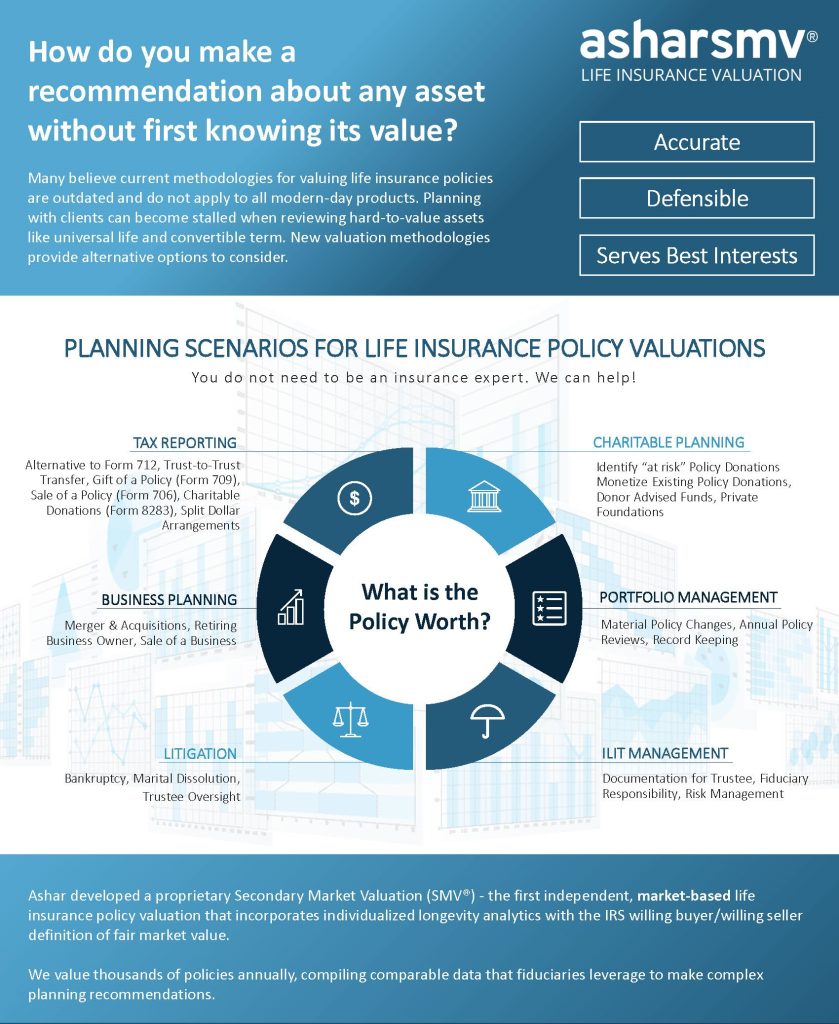

You likely discuss the value of your client's real estate, trusts, businesses, retirement funds, and other equities at length. But what about their life insurance policy? Life insurance policies are assets and should be valued like any other piece of property.

The value of a policy can affect estate taxes and deductions, as well as a client's decision to keep, surrender, or sell a policy. Once the policy has done its job and the original purpose of the coverage has diminished, an accurate valuation can help clients make an informed decision about whether to continue allocating funds to the premium, surrender the policy for cash value, or explore the option of monetizing it for more than cash value to help fund other planning, like retirement, investments, caregiving, and even charitable donations.

ALTERNATIVE TO SURRENDER: In the right circumstances, a policy can be exchanged for more than the cash value. A life settlement is the sale of an existing life insurance policy for more than the cash surrender value and less than the face amount. This solution eliminates future premium obligations and creates liquidity for other planning needs.

UNDERFUNDED POLICY IN AN ILIT

June's advisor reviewed the value of all her assets, including her life insurance policy. Read June's Story

Schedule a call to discuss how we help you integrate life settlements and life insurance valuation into your client conversations, share tools that will help you get started, and calculate the opportunity for your firm and clients.

Clients have questions. We have answers.

Learn more about how we serve financial professionals and fiduciaries.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.