As a financial advisor with senior clients, you frequently help them plan for retirement, determine how to pay for long-term care, and advise family members on choosing a guardian or power of attorney.

Unfortunately, another situation that may come up with your older clients is elder financial abuse. Perpetrated through coercion, deception, or by simply taking advantage of a person’s diminished physical or mental capacity, elder financial abuse can encompass a multitude of behaviors: theft of valuable items, forged signatures on legal documents, or forced access to bank accounts, among other things.

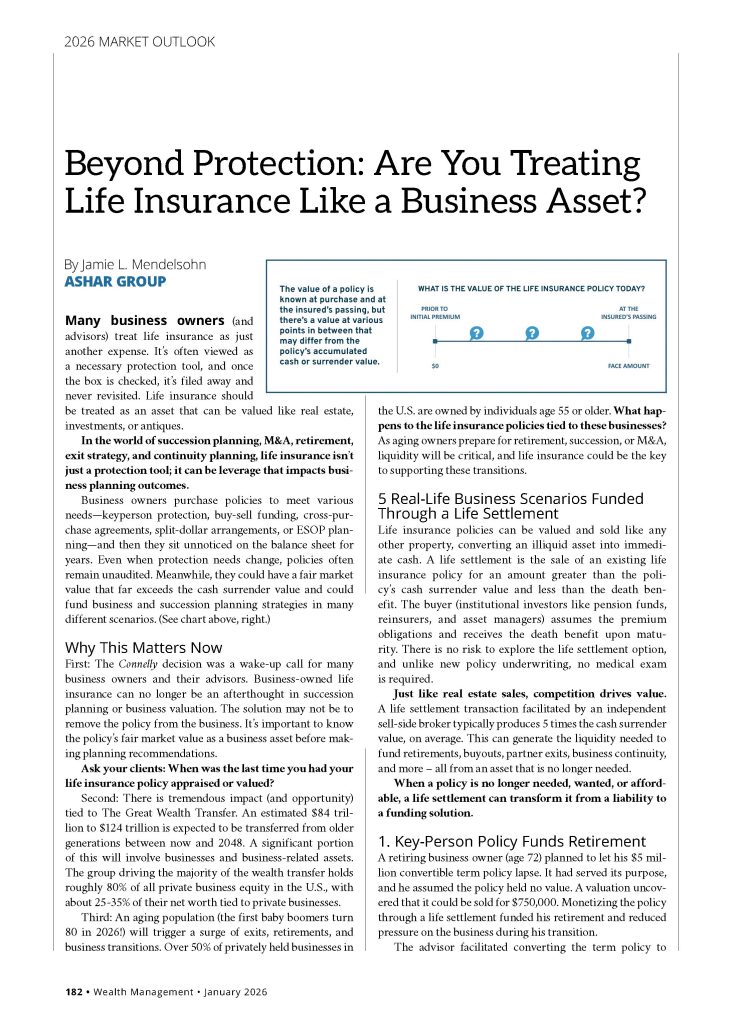

Many business owners (and advisors) treat life insurance as just another expense. It’s often viewed as a necessary protection tool, and once the box is checked, it’s filed away and never revisited. Life insurance should be treated as an asset that can be valued like real estate, investments, or antiques. In the world of succession planning, M&A, retirement, exit strategy, and continuity planning, life insurance isn’t just a protection tool; it can be leverage that impacts business planning outcomes.

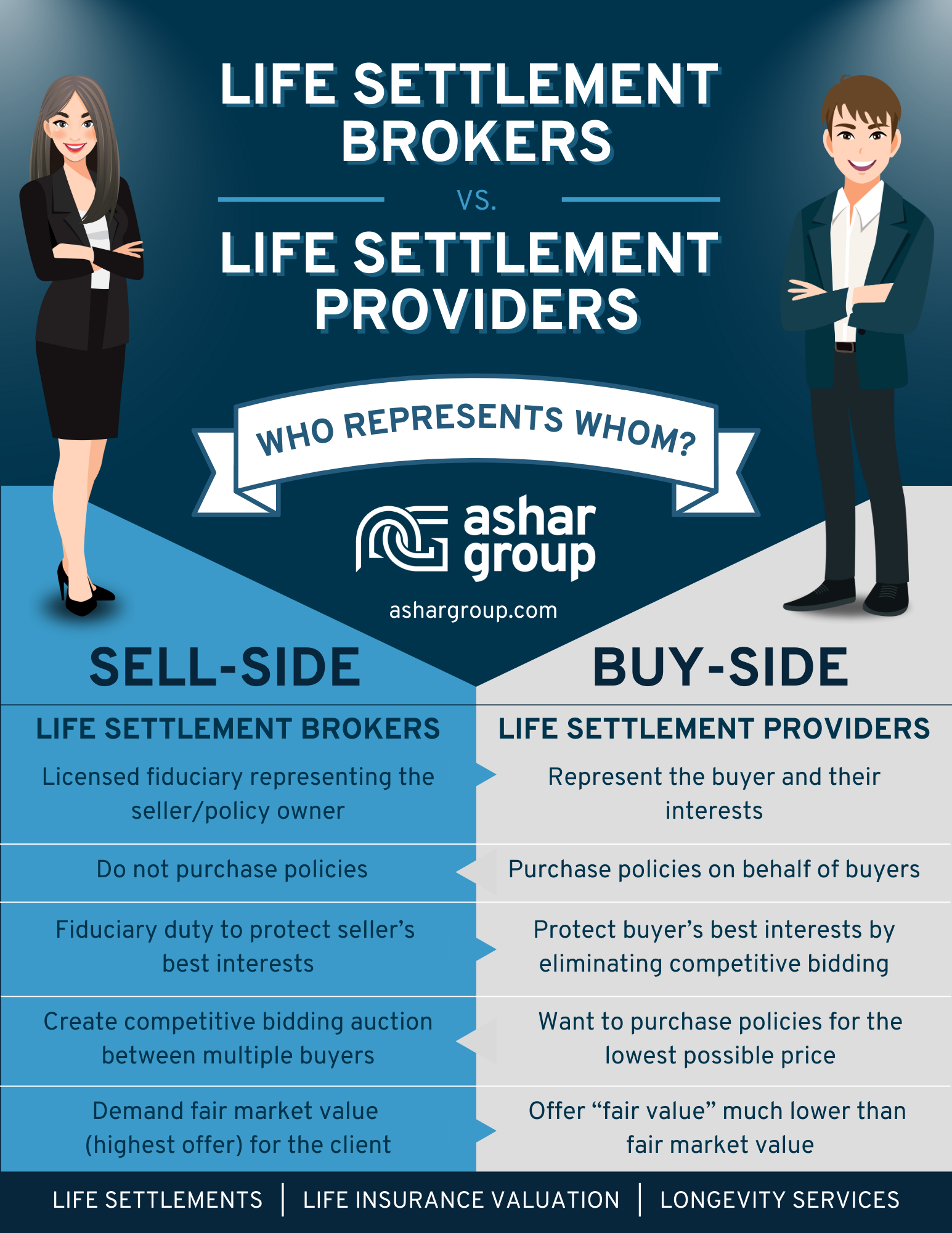

Ashar Group is a nationally licensed sell-side life settlement firm that protects policy owners’ best interests by facilitating a competitive policy auction to deliver the best value to sellers. We are an independent resource for fiduciary advisors and their clients, specializing in life insurance valuation for planning purposes. Ashar Group does not sell life insurance, manage assets, or purchase policies.

Gray divorce is defined as a divorce or separation that occurs later in life, typically at age 50 or beyond. Studies have shown that divorce rates for those aged 65 and older have tripled since 1990.

This phenomenon often involves financial challenges far greater than those in earlier-life divorces. In general, there are often more assets to consider, but one in particular is life insurance. Life Insurance policies are valuable financial assets, not just protection vehicles, and should be valued as part of the asset review in divorce.

Is the coverage still needed?

If one spouse still needs income protection, or if the policy is intended to secure support obligations, such as alimony, pension sharing, or maintenance, the policy may still be essential.

Is the insured still insurable?

In cases of gray divorce, health changes may be a factor to consider. If the insured is now uninsurable, the existing policy may be even more valuable to keep.

If it is determined that the policy should remain in force, the divorce settlement should outline policy ownership, premium obligations, and beneficiary designations.

Does the original policy need to be replaced?

In some scenarios, ownership and beneficiary structures become unworkable in divorce, generally when spouses do not want to retain any financial ties. In these cases, new separate policies might replace joint or survivorship policies.

Life insurance should be valued before lapse, surrender, or any material changes are made to the policy.

Does the policy have value over cash surrender value?

In situations of replacement or where there is no longer an economic need, neither spouse wishes to keep paying premiums, or the policy is underfunded, it may be decided to cancel the existing policy. Before the policy is lapsed, surrendered, or materially changed, it should be reviewed for fair market value.

Especially in a gray divorce, because the insured(s) are older and may have health issues, the policy may have significant value above its cash surrender value if sold as a life settlement.

A life settlement is the sale of an existing life insurance policy for more than the cash value and less than the death benefit. All types of Universal Life and Convertible Term policies are very attractive to institutional buyers in the secondary market.

In 2022, life settlements generated 5x more than the cash surrender value on average.

Selling a life insurance policy should be explored when the need for coverage no longer exists, a life settlement can generate more than the cash value, or funds are needed for current financial needs.

Representation is essential when considering a life settlement. Many resources advertising on TV are direct buyers looking to purchase the policy for the least amount possible. To guarantee the best offer, work with an independent, sell-side advisory firm whose fiduciary duty is to the policy owner.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients, specializing in life insurance valuation for planning purposes.

For some charities, life insurance is a taboo subject, and they often surrender donated policies without any analysis. With approximately 51% of the U.S. population owning life insurance, it’s too large an asset class to omit from charitable planning discussions with donors, particularly considering the tremendous opportunities.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients, specializing in life insurance valuation for planning purposes.

...And the youngest of them turn 61 this year.

As the financial landscape continues to evolve, so too must the approach of today's financial advisor. Gone are the days when retirement planning stopped at age 85. With more clients living into their 90s and beyond, comprehensive planning must now stretch across longer time horizons. The means anticipating new risks, uncovering new opportunities, and using tools like life settlements to help clients maximize their long-term financial security.

Advancements in healthcare, improved lifestyles, and greater awareness of wellness have all contributed to a significant rise in life expectancy. According to a recent article, many clients - especially those in higher-income brackets - have a very real chance of living into their 90s or even longer. This longevity shift can strain retirement income projections and long-term care strategies if not properly considered.

Advisors can no longer plan to age 85. Retirement strategies must now account for 30 to 40-year retirements, demanding smarter planning, more flexible assets, and more nuanced conversations with clients.

Living longer is a gift - but it comes with a price tag. Increased healthcare costs, long-term care, inflation, and the risk of outliving assets are very real concerns for retirees. Clients fear becoming a financial burden to their families or having to sacrifice quality of life late in retirement.

It's crucial for advisors to start the longevity conversation early. Educating clients about the financial realities of extended lifespans can help them make more informed, proactive decisions. It's also a natural segue into evaluating underutilized assets that could support their long-term needs, such as life insurance policies.

An often overlooked but powerful tool in the longevity toolkit is a life settlement - the sale of an unwanted or unneeded life insurance policy for a lump sum that exceeds the cash surrender value (and is less than the death benefit). For clients in their 70s, 80s, and even 90s, this can be a strategic move that unlocks hidden value in a policy that no longer fits their goals.

Consider a client who took out a large policy to protect a growing family or business, but now finds those needs have changed. Instead of lapsing the policy or surrendering it for minimal value, a life settlement can provide immediate funds that support long-term care needs, retirement lifestyle, or estate planning goals.

Clients are often unaware of the option (or are duped by direct-to-consumer advertising), and their advisors are in the best position to educate them. When integrated into a comprehensive plan, life settlements can:

Advisors who ignore the longevity risk are not just missing a piece of the puzzle, they are missing a core component of modern financial planning. By acknowledging longer lifespans and incorporating strategies like life settlements, advisors can offer peace of mind and financial confidence that lasts a lifetime - and beyond.

As the industry continues to shift, advisors will stand out not just for managing assets, but for managing expectations and delivering solutions that evolve as life gets longer.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

In a nutshell, your client can have some serious health issues that disqualify them for new insurance, but still have a relatively long life and therefore not qualify for a life settlement. It's because insurance carriers are underwriting different risk factors at policy issue compared to institutional buyers who purchase existing life insurance policies.

Life insurance carriers are concerned about mortality risk - the risk of the insured passing too soon. Their underwriting places emphasis on health and lifestyle debits to determine life expectancy. They look at the worst-case scenario.

Insitutional life settlement buyers are concerned about longevity risk - the risk of the insured living too long. Their underwriting looks at the debits, but also health and lifestyle credits. They focus on the best-case scenario.

There are 2 main factors institutional buyers consider when determining whether the purchase of an existing life insurance policy is a good investment:

It's all about the math. In some cases, high premiums can kill a life settlement deal for an insured with health issues that would lead to a decline for new insurance. For example, if the policy has an 8%-10% premium ratio (annual premium/face value), then the life expectancy of the insured would have to be shorter for it to be attractive to buyers. Conversely, a policy with a low premium ratio (1%-3%) allows for a longer life expectancy and is still considered a good investment for buyers.

The best way to ensure your client gets the most for their unneeded/unwanted life insurance policies in a life settlement is to execute an auction that forces buyer competition. Buyers are looking for the best rate of return for the investors they represent. Just like with real estate, when buyers compete, the client (and the advisor) win!

Ashar Group is a nationally licensed independent seller’s representative. We sit on the same side of the table as the planning professional and their client, ensuring the policy owner’s best interests are protected. Because we don’t purchase the policies, our sole responsibility is to the client. Through our auction platform, we create competition between buyers to ensure policy owners are getting the best offer.

PRACTICE TIP: Ask these three questions of your life settlement resource to ensure your client has independent representation in the life settlement transaction:

Learn more about the difference between sell-side and buy-side.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

Over the past two decades, a reliable secondary market for life insurance has emerged with an auction process that can uncover a policy’s fair market value (FMV), which can be vastly different from its current cash value. Life insurance is an asset your clients own. When was the last time it was appraised? Like your clients’ other ordinary property, it is important to value their life insurance property before they materially change it or terminate it.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

By Jamie L. Mendelsohn | EVP | Ashar Group

Article published in 2025 Wealth Management Market Outlook

By evaluating clients’ existing policies, advisors can uncover opportunities to convert underperforming or unneeded life insurance into liquid assets through the life settlement solution that can be reinvested to align with clients’ broader financial goals.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients, specializing in life insurance valuation for planning purposes.

Likely, you discuss real estate, trusts, businesses, retirement funds, and other equities with your clients at length. But what about their life insurance policy?

A life settlement is the sale of an existing life insurance policy to an institutional investor for more than the cash surrender value and less than the death benefit. The funds from a life settlement can be used for other planning needs - investments, new insurance on healthier insureds, retirement, charitable donations, and much more.

SUCCESS STORIES

We value thousands of policies each year. View more more life settlement success stories here.

Not every life insurance policy will qualify, but the ones that do can be sold for much more than their cash surrender value.

Try our Life Settlement Probability Calculator to determine if your client's policy could qualify.

Many financial professionals feel they don’t know enough about life insurance or life settlements to discuss this solution with their clients. We're here to help answer your questions about the market and guide you and your client through the process.

Complete the form below and a member of our Strategic Partnerships team will reach out to schedule a time for your life settlement market update with one of our experts.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

June, an 84-year-old widow, saw something in a television ad that piqued her interest. After husband Frank passed away two years ago from a long battle with heart disease, June found herself in an assisted living facility, burdened by mounting medical bills. While knitting a baby blanket for her new great-granddaughter one afternoon, a captivating commercial flickered across her TV screen, promising relief from her financial worries. It touted the option of selling her life insurance policy for cash through something called a life settlement. Intrigued, she set aside her knitting and jotted down the contact information.

Why did June consider a life settlement? As June pondered the possibility, she realized she no longer had a pressing need for the policy. Her children were grown and financially stable, yet she was still shelling out hefty premiums to maintain coverage. "Why not explore this further?" she thought. With a simple phone call to the number from the commercial, June received a cash offer of $75,000 in less than 48 hours. The offer was three times greater than the $25,000 cash surrender value of her policy.

The offer seemed almost too good to be true, stirring both excitement and unease within June. She felt pressured to make a quick decision and was unfamiliar with the company pushing the deal. Was she being targeted by another financial scam aimed at unsuspecting seniors?

Seeking clarity, June turned to her trusted advisor, Michael, who assured her it wasn't a scam but urged caution. He explained that many direct-to-consumer marketers aim to purchase policies at a steep discount, prioritizing their interests over the sellers'. Instead, Michael suggested consulting a life settlement broker with a fiduciary duty to secure the best deal for June.

Michael contacted Ashar Group, a reputable firm specializing in appraising life insurance assets and facilitating life settlements. With Michael's guidance and Ashar Group's expertise, June embarked on a journey to maximize the value of her policy. Together, they compiled compelling information to present through the policy auction, where multiple buyers would compete for the opportunity to purchase her policy. Just like in a real estate bidding war, this competitive environment drove up the value of June's policy.

Though the process took longer than the initial 48 hours, June felt no pressure to rush, and the outcome was beyond her wildest expectations. The auction yielded 14 separate bids, with the winning offer coming in at a staggering 19 times higher than the cash surrender value. What's more, the winning bid came from the very same buyer who had initially offered her only three times the cash surrender value. The key to this remarkable outcome? The competition created by the auction process, coupled with thorough underwriting, uncovered the true value of June's policy.

The moral of the story is clear: Seniors should exercise caution when tempted by direct-to-consumer life settlement ads on TV and social media. Instead, entrust their interests to a nationally licensed life settlement broker like Ashar Group, ensuring they receive the best possible outcome.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

{kind=link}