Practical Guide for Financial Professionals

Historical Reference

The option to sell a life insurance policy became possible after a 1911 U.S. Supreme Court Ruling in Grigsby v. Russell deemed life insurance personal property with transferable value.

It wasn’t until the 1980s, during the AIDs epidemic, that policyowners began selling policies as a way to pay for healthcare and end-of-life expenses. These transactions were known as viatical settlements. Today, a viatical settlement refers to a policy sale in which the insured has a life expectancy of two years or less.

In the early 2000s, as life settlements began to gain traction as a planning tool, the IRS remained uncertain about how to tax these transactions. The first revenue ruling (Rev. Rul. 2009-13) treated a policy sale differently from a policy surrender and required a calculation that deducted the cost of insurance (COI) from the cost basis (the policyowners’ total investment in the asset), making it difficult for practitioners to calculate taxes.

Tax Cuts and Jobs Act 2017 (TCJA)

The TCJA clarified that a policyowner’s basis is not reduced by the cumulative cost of insurance charges to determine gain on a policy sale. This change results in a higher basis and a reduction in tax liability, making the outcome more favorable to policy sellers.

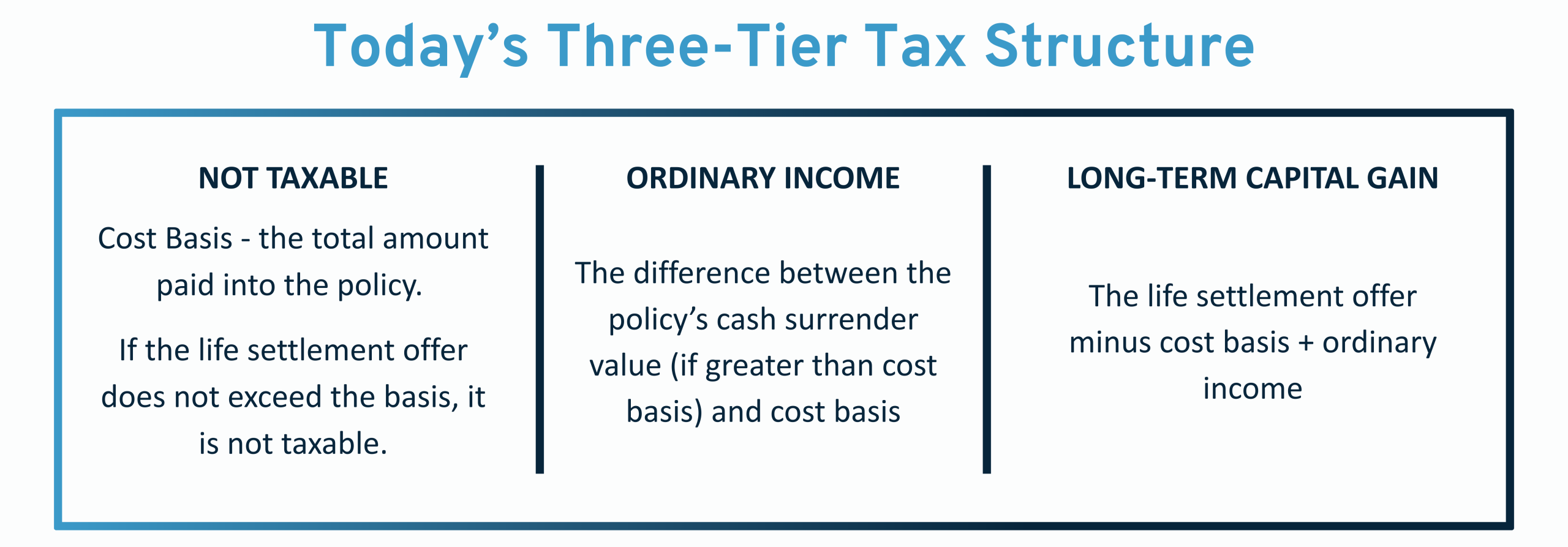

Revenue Ruling 2020-05

Further updates in January 2020 made the tax treatment of selling a life insurance policy consistent with that of surrendering a policy.

Ashar Group does not provide tax advice. Policyowners and advisors should consult with qualified tax and legal experts regarding any life settlement transaction and before making any tax-related decisions.

This is provided for informational and educational purposes only and is not intended to constitute tax, legal, accounting, investment,

or financial advice. The tax treatment of life settlement transactions depends on the specific facts and circumstances of each case

and is subject to change under applicable law. Policyowners and advisors should consult with qualified tax and legal experts

regarding any life settlement transaction and before making any tax-related decisions.