Broker-dealers, banks, ILIT trustees, insurance carriers, and planners with a fiduciary duty understand that part of protecting clients' best interests means offering all the available options and recommendations to help clients meet their planning goals. When it comes to life insurance, many factors affect whether a policy still meets the original purchase goal. As policy owners age, they outlive their original planning goals, interest rates affect policy performance, and life situations change. Therefore, the need for their life insurance coverage may change too. Sometimes that means exiting a life insurance policy that no longer serves a positive financial purpose.

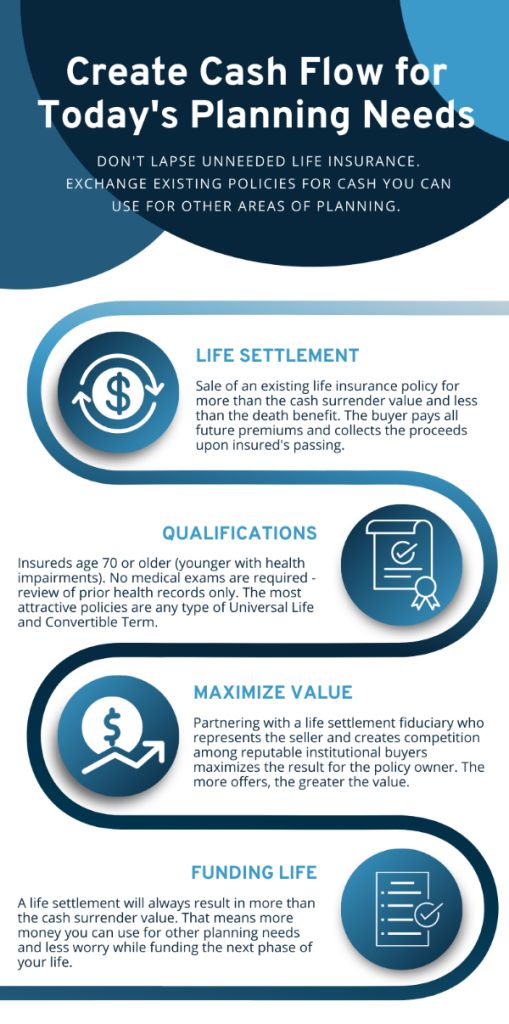

There is a valuable alternative to lapse or surrender. A life settlement is a buyout of an existing life insurance policy for more than the cash surrender value and less than the death benefit.

Over time, compliance officers have come to recognize that if life settlements are pursued for the right reasons, after a thorough review of all non-forfeiture options and suitability, a life settlement could very well be in clients' best interests. It is a viable exit strategy that should be disclosed in a comprehensive policy review in partnership with a resource that offers a compliance-centric process. However, broker-dealers do not just allow life settlements carte blanche. They put strict procedural guardrails in place to protect the company and their representatives from liability risk.

When you or your client encounter marketing by a life settlement company, they may all sound the same. It is exceedingly difficult for even the most experienced advisors to differentiate between a company representing their client's best interests and one representing the buyers. There are multiple factors compliance officers consider when selecting a life settlement company. However, there are common mistakes to avoid that revolve around ensuring that your clients receive independent and knowledgeable representation that protects their best interests.

Ensuring the life settlement company has a fiduciary duty to your client, the policy owner, is the most critical factor in approving a compliance-centric resource.

There are key elements that compliance officers look for when completing their due diligence in the approval of a life settlement partner.

Although compliance officers are responsible for protecting the best interests of the company they represent, they have historically hesitated to approve life settlements for advisors to offer as an option to clients. Ninety percent of states regulate settlements, alleviating past concerns and helping to integrate this solution into mainstream planning. Broker-dealers do not advertise or promote life settlements, so we encourage advisors to check with their compliance department to ask if they have an approved life settlement resource.

Over the past 20 years, we have undergone numerous lengthy due-diligence processes and assisted in designing compliance-centric workflows for many of the largest nationally recognized broker-dealers. Discover how we're different by design.

Ashar Group is a nationally licensed life settlement firm that acts as a fiduciary to protect the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

Your client’s life insurance policy may be the most valuable asset they own.

Seniors in retirement often drop their life policies. The reasons are many; the original need may no longer exist, they may need to eliminate expensive premium payments, or they just need some additional liquidity to help with medical costs and retirement needs. There could be a better way...

A life settlement is the sale of an existing life insurance policy for more than the cash surrender value and less than the death benefit.

Five Common Life Settlement Scenarios:

Who has the best chance of qualifying for a life settlement?

Anyone age 65 or older who has developed health issues since their policy was issued and owns a universal life or convertible term insurance policy has a high probability of benefiting from selling their policy. Policies with a death benefit of $250K or more can qualify. Even policies used in estate planning and business protection with death benefits from $2M - $100M can qualify. Younger policy owners with serious chronic illnesses can also explore the life settlement option. There are many scenarios where a client could qualify for a life settlement.

PRACTICE TIP: Never surrender a life insurance policy without first checking for life settlement value!

Ashar Group is a nationally licensed life settlement firm that acts as a fiduciary to protect the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

Responding to online advertising and generic value calculators can mislead client expectations. Many things in life rarely come about; when this happens, the average person doesn’t have the knowledge to make a good decision. This can be true for financial professionals and consumers alike.

Understanding life settlements is one of those things. Where do advisors and consumers go to find the answers to questions about life settlements? If you Google life settlements, you will come up with 152,000,000 results. Even if you zoom past all the paid ads, you are still left with an abundance of contradictory opinions and information. Consumers are particularly vulnerable when they respond to direct-to-consumer TV commercials and social media ads about life settlements.

If you’re an advisor, who would you listen to, and how would you know if you can trust them to serve the best interests of your clients? Most of these ads come from life settlement lead generation companies and life settlement providers that represent the best interests of buyers wishing to purchase existing life insurance policies at a highly discounted price. It’s a good deal for the buyer but a bad deal for your clients. Furthermore, it’s almost impossible to use Google to determine whether you’re working with a licensed life settlement provider representing the buyer’s best interests or a licensed life settlement broker with a fiduciary duty to represent the best interests of the policy owner selling the policy.

This is precisely why attorneys, CPAs, CFPs, RIAs, and client-centric life insurance professionals do not rely on Google, social media, or television ads to determine who they should trust to help their clients. They use a more comprehensive due diligence process to protect themselves and their clients.

The strategy behind life settlement calculators

Most online life settlement platforms connect policyholders directly or indirectly with licensed providers that represent the best interests of buyers. They aim to lead your client to provide information by completing their life settlement calculator, then give them an arbitrary value and engage them in conversation. This is a problem for your client because the value indicated is, at its best, only a guess. The minimal output from a calculator is rarely accurate, and the potential offer is changed after additional medical, financial, and policy information is obtained. This misleads your client and forces them to lower their expectations. Often a highly discounted offer will be presented to your client based solely on the information provided on the calculator, and the deal can be closed quickly. Too quickly!

Moving too fast in life settlements can come with some inherent risk for you and your clients. If your client is involved in a life settlement process emphasizing speed, you might suggest they tap the brakes and determine if they are sitting on the wrong side of the negotiation table.

Bottom line: Complex transactions that require sophisticated underwriting and a negotiation process take time. There are only two licensed entities that sit at the negotiation table. Life Settlement Brokers represent your client’s best interests, and Life Settlement Providers represent the buyer’s best interests. Fast life settlements are risky. Slow down on the front end to verify that your client is represented by a nationally licensed life settlement brokerage firm experienced in case design and conducts a transparent policy auction between multiple providers to drive more value to your client. They will be glad you did!

Ashar Group is a nationally licensed life settlement firm that acts as a fiduciary to protect the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes. Contact us today.

Ashar Group has created a special checklist for tax season that helps you conduct a new and timely discussion that strengthens your current relationships and opens the door to new ones.

Most tax practitioners are unaware that existing life insurance policies can provide a value significantly higher than the cash surrender value offered by the issuing insurance carrier.

“Almost 85% of term policies fail to pay a death claim; nearly 88% of universal life policies ultimately do not terminate with a death benefit claim. In fact, 74% of term policies and 76% of universal life policies sold to seniors at age 65 never pay a claim.”

Wharton School Study by Daniel Gottlieb and Kent Smetters

What happens to all those policies that were put in place to protect families and businesses? They are lapsed or surrendered. Most of those policies are dropped by senior clients in financial transition. The reasons are many. Their policy may no longer be needed for estate tax planning, they are outliving their coverage, the policy is too expensive to maintain, a business owner is retiring, or they are going through bankruptcy proceedings or divorce proceedings. Often, they simply want to apply any cash they can obtain from the policy and use that cash - and the ongoing premiums they have been paying - to other aspects of their financial plan. They may need extra cash for medical or caregiving expenses, donate money to charity, or simply maintain their standard of living during retirement. Furthermore, many tax advisors and consumers are unaware of the additional value that can be obtained through a life settlement.

What can tax professionals and financial advisors do to help?

It’s simple, all you must do is be in the right place at the right time before your client decides to lapse or surrender an existing life insurance policy. That’s where our Tax Planning Checklist for Existing Life Insurance comes in. Tax season is the perfect time to reach out to your clients and tax professionals and ask them the questions on the tax planning checklist. This creates awareness about options that are available that could have a significant impact on decisions that they make when considering dropping their existing life insurance coverage.

We’ll be at Finseca in D.C.

Please stop by the Ashar Group booth #201 to get access to the Tax Season Checklist and options to co-brand this checklist.

Over time, the need for life insurance coverage naturally changes. While life insurance can sometimes be the largest asset a client owns, it’s rarely reviewed for fair market value like other assets, including real estate, art, and jewelry. This results in clients making uninformed decisions, missing lucrative planning opportunities, and paying unnecessary premiums.

We all know the advantages of early detection when it comes to identifying health risks. We never want to hear the doctors say, “If only we had caught this sooner…”.

Your automobile is equipped with all sorts of warning mechanisms to detect a problem before it turns into a costly repair.

Your children’s report cards provide early detection of a drop in grades before your child needs to repeat a grade.

Your annual dental visits for cleaning and x-rays help detect cavities before they turn into serious problems.

What about existing life insurance policies that your clients currently own? When was the last time you had your client’s existing life insurance appraised to detect all available planning options?

Right now, you have clients in financial transition. Whether it is retirement, selling a business, divorce, bankruptcy, or simply outliving their financial plan, your clients ask, “What are my options?” Is it best for me to keep paying premiums, change my coverage, surrender my policy, or sell my policy for its life settlement value? If you aren’t answering these questions, someone else will. This leaves your clients and the relationships/trust you’ve built with them vulnerable and in jeopardy.

There are many reasons to consider an Early Detection Valuation to explore the suitability of maintaining existing life insurance coverage. You don’t need to be a life insurance expert or hold a license to consider a valuation or a life settlement. We’re here to help. We’re a qualified appraiser of life insurance for estate and tax planning, charitable donations, and other aspects of financial and retirement planning. Contact us today.

Ashar Group is a nationally licensed life settlement firm that acts as a fiduciary to protect the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, management assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

Life insurance can be the largest unmanaged asset a client owns. Policy owners allocate significant liquidity on an ongoing basis, often long after they transition out of the original need that the policy was put in place to protect. Discussing the opportunity to take an illiquid asset and monetize it when clients are going through a financial transition, whether to fund business, retirement, long term care or charitable endeavors, can be a powerful client conversation.

Learn more about the state of the market from one of the nation's leading experts on life insurance valuation and life settlements.

The path you choose will determine how much value created ends up on the policy owner/sell-side of the negotiation table versus the buy-side. One wrong turn can take you and your client down a path that enhances investor returns at the expense of providing more value to your client. Right now, policy owners are being bombarded with life settlement marketing that can often blur the lines between truth and fiction. It's important to help your clients make an informed decision by choosing a life settlement partner who is 100% aligned with you and your client.

PRACTICE TIP: SECURING INDEPENDENT REPRESENTATION FOR YOUR CLIENT IS THE CORNERSTONE OF A SUCCESSFUL LIFE SETTLEMENT.

An existing life insurance policy, including convertible term insurance, may contain significant value beyond the cash surrender value (CSV) that can be accessed through a life settlement. A life settlement is the sale of an existing life insurance policy for an amount greater than the CSV but less than the death benefit. How much value your client receives is dependent on which life settlement company is chosen to represent them. The good news is that life settlements are highly regulated and require licensing that distinguishes between a seller's representative and a buyer's representative. Securing independent representation for your client is the cornerstone of a successful life settlement.

There are only two entities licensed to handle life settlement negotiations. One represents the seller, the other represents the buyers. Licensed life settlement brokers are fiduciaries to your client, the policy owner. Their sole responsibility is to represent the policy owner in the life settlement transaction and obtain the best offer based on your client’s situation and needs.

One wrong turn can take you and your client down a path that enhances the buyer's returns at the expense of providing more value to your client.

On the buy side, life settlement providers are licensed to represent the best interests of the purchaser. Most advisors are unfamiliar with the term provider, which is often conflated with the term "buyer". As a result, advisors often unknowingly end up on the wrong side of the negotiation table, working with a provider. Consumers are even more vulnerable because of increased consumer-direct ads from providers on television and social media aimed at disintermediating the policy owner's representation. If your client responds to an advertisement and gets involved with a “direct buyer,” they are dealing with a provider.

PRACTICE TIP: A BROKER-MANAGED LIFE INSURANCE POLICY AUCTION FORCES COMPETITION AMONG BUYERS TO ENSURE THE POLICY OWNER GETS THE BEST OFFER FOR THE POLICY.

NOTE: Only choose one broker that forces buyer competition. When purchasers receive information from two or more sources, control of the case is lost, often resulting in a discounted offer to the seller. It also ensures the protection of sensitive client information. A secure policy auction will ensure your client's policy will be reviewed by all available buyers.

Due Diligence: Determine if a life settlement company is on the buy-side or sell-side

Ask potential life settlement resources these two questions:

IMPORTANT: insurance agents who want to receive a commission from a life settlement must first be appointed as a life settlement broker. They may complete one or two life settlement cases per year. They do not have the staff, national licensing, or expertise to run the policy auction. Make sure your resource is a nationally licensed life settlement broker. Fiduciaries do not take commissions but can charge fees for life insurance valuation and other services provided by a life settlement broker.

Bottom line: There are only two licensed entities that sit at the negotiation table. Life Settlement Brokers represent your client’s best interests, and Life Settlement Providers represent the buyer’s best interests. The first step is to verify that the life settlement company you choose to help your client is a seller’s representative. Starting on the right foot will have a big impact on the value your client receives.

____________________________________________________________________________________

Ashar Group is a nationally licensed life settlement broker that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

Use our life settlement probability calculator to determine potential opportunities, or contact us today to learn more about the life settlement solution.

Divorce rates are on the rise - but not among younger couples, as one might expect. Instead, the increase is among couples who are ages 50 and older. According to the US Census Bureau, divorce rates among adults ages 55 to 64 are about 43% and have increased since the 1990s.

While divorce at any age is a complicated and emotional process, divorcing when you're over the age of 50 has some bleaker financial consequences than it might for a 25- or 30-year-old. That's because divorce almost always has a negative effect on a person's lifetime financial state. If you're close to retirement when you divorce, there's much less time to recover.

There are a couple of reasons for this. Women are more financially independent, which allows them to divorce without facing as stark of a financial picture as they once did. Additionally, as longevity increases, the overall length of marriage is longer. This on its own puts couples at a higher risk for divorce. Here are a few things to consider if you're among one of the many adults getting divorced after age 50.

Retirement accounts are usually considered marital property.

Preparing for retirement takes decades of planning and saving by contributing to a 401(k) or IRA. In most states, funds that you contributed to a retirement account over the course of your marriage are considered property and assets. This means that when you divorce, that money gets split between the two of you.

What was once enough to cover a single mortgage and utilities for a single household, might not be enough now that it must cover two separate households. The implications of this are profound, including the possibility of delaying retirement a few years or working part-time while retired.

Does keeping the house make sense?

During a divorce when the house is nearly or fully paid off, is keeping the house the right decision for either party? The house has a value, which means that your ex-spouse will receive some property equal to that value, and it might be retirement or savings accounts, future payments until that amount is met, or a life insurance policy.

In addition, a home comes with considerable costs that might stretch your already reduced retirement savings beyond their limit. Such as repairs, homeowner's insurance, and more.

Alimony is typically granted if the marriage has been a long one.

When marriages last a specific length of time, you can expect a form of alimony or spousal support to come into play. Divorces that end shorter marriages often include some kind of payment for a short time to assist the less well-off spouse in recovering.

Separating from your spouse can wreak havoc on not only your emotional life but your financial one as well. If you are going through this difficult event, thinking about money is probably the last thing you want to do - however, if you don’t, you could find yourself in a highly precarious financial situation once the divorce is final.

If you retain ownership of a life insurance policy during divorce negotiations that has become unnecessary, or a burden, you may want to consider a life settlement. Selling your policy for an amount greater than the cash surrender value can provide a significant liquidity event allowing you to bridge the gap in earnings.

Life settlements are an underutilized option that can be very helpful for seniors in certain circumstances. To learn more, read more about how this option can be beneficial for policy owners, or contact us today.

Retirement is more than just turning in your notice at work and packing up your desk. Beyond looking at your finances, there is other planning that should go into the decision to retire.

Define "retirement".

What does retirement look like to you? Are you sitting on the beach somewhere or traveling the world? Many people know what they are retiring from, but they don't always think about what they are retiring to. Write down your retirement goals - don't say just "travel" but instead "cruise to Cancun" or "bus tour in European countries".

Many people find themselves in financial trouble after retirement because they didn't weigh the opportunity costs of their ideal life: they'll move to the west coast for good weather but rack up high travel costs to see their grandchildren in the Midwest every other month, for example.

Be realistic about costs of hobbies: many financial planners predict you'll spend less in retirement than you did previously, but a pricy hobby (like college classes or sailing) can often derail the best-laid budget.

Improve your health.

Just before your retirement date, it is best to see all your healthcare providers. While at your appointment, ask your providers to help develop a plan to keep you fit and alert during your retirement years. Commit to the suggestions, whether they are eating two green veggies a day, walking around the mall a few times a week, flossing, or doing brain games to stay sharp.

Find any opportunities for added income.

Look for opportunities to turn your hobbies into profit. You can sell your crocheted blankets to friends, teach piano to the neighborhood children, or turn your business skills into a consulting job. Many people get bored after a few months of retirement and actually prefer partial-retirement, in which they pick up part-time jobs. Remember, retirement doesn't have to mean not working; it's just having the freedom to do what your want when you want.

If you don't want to continue working during retirement, another option is to sell your unwanted or unneeded life insurance policy in a life settlement. A life settlement can create a significant liquidity event that can fund your retirement goals; however they look. To see if your policy could potentially qualify for a life settlement, take our Policy Value Questionnaire. For more details about life settlements and policy valuations, contact us today.