In a nutshell, your client can have some serious health issues that disqualify them for new insurance, but still have a relatively long life and therefore not qualify for a life settlement. It's because insurance carriers are underwriting different risk factors at policy issue compared to institutional buyers who purchase existing life insurance policies.

Mortality Risk vs. Longevity Risk

Life insurance carriers are concerned about mortality risk - the risk of the insured passing too soon. Their underwriting places emphasis on health and lifestyle debits to determine life expectancy. They look at the worst-case scenario.

Insitutional life settlement buyers are concerned about longevity risk - the risk of the insured living too long. Their underwriting looks at the debits, but also health and lifestyle credits. They focus on the best-case scenario.

Factors that Influence Calculations

There are 2 main factors institutional buyers consider when determining whether the purchase of an existing life insurance policy is a good investment:

- What is the cost of ongoing premiums? Buyers favor policies such as universal life or convertible term policies because they can manipulate the annual cost by paying the minimum premium needed to keep the policy in force. If the policy you present has high premiums or static premiums, it makes it more challenging to get offers.

- How long will premiums have to be paid? Translation: How long is the insured expected to live? Factors such as wealth, education, travel, strong relationships, family history of longevity, habits, and access to quality health care have all been proven to extend life expectancy. Also, life expectancy gets longer as you reach certain age milestones. If your client lives to age 65, then there is a good chance that his/her life expectancy increases to age 83-85. If the same client lives to age 70, then there's a better chance of getting to age 90, and so on.

Relationship Between Premium and Life Expectancy

It's all about the math. In some cases, high premiums can kill a life settlement deal for an insured with health issues that would lead to a decline for new insurance. For example, if the policy has an 8%-10% premium ratio (annual premium/face value), then the life expectancy of the insured would have to be shorter for it to be attractive to buyers. Conversely, a policy with a low premium ratio (1%-3%) allows for a longer life expectancy and is still considered a good investment for buyers.

Maximizing Life Settlement Value with a Policy Auction

The best way to ensure your client gets the most for their unneeded/unwanted life insurance policies in a life settlement is to execute an auction that forces buyer competition. Buyers are looking for the best rate of return for the investors they represent. Just like with real estate, when buyers compete, the client (and the advisor) win!

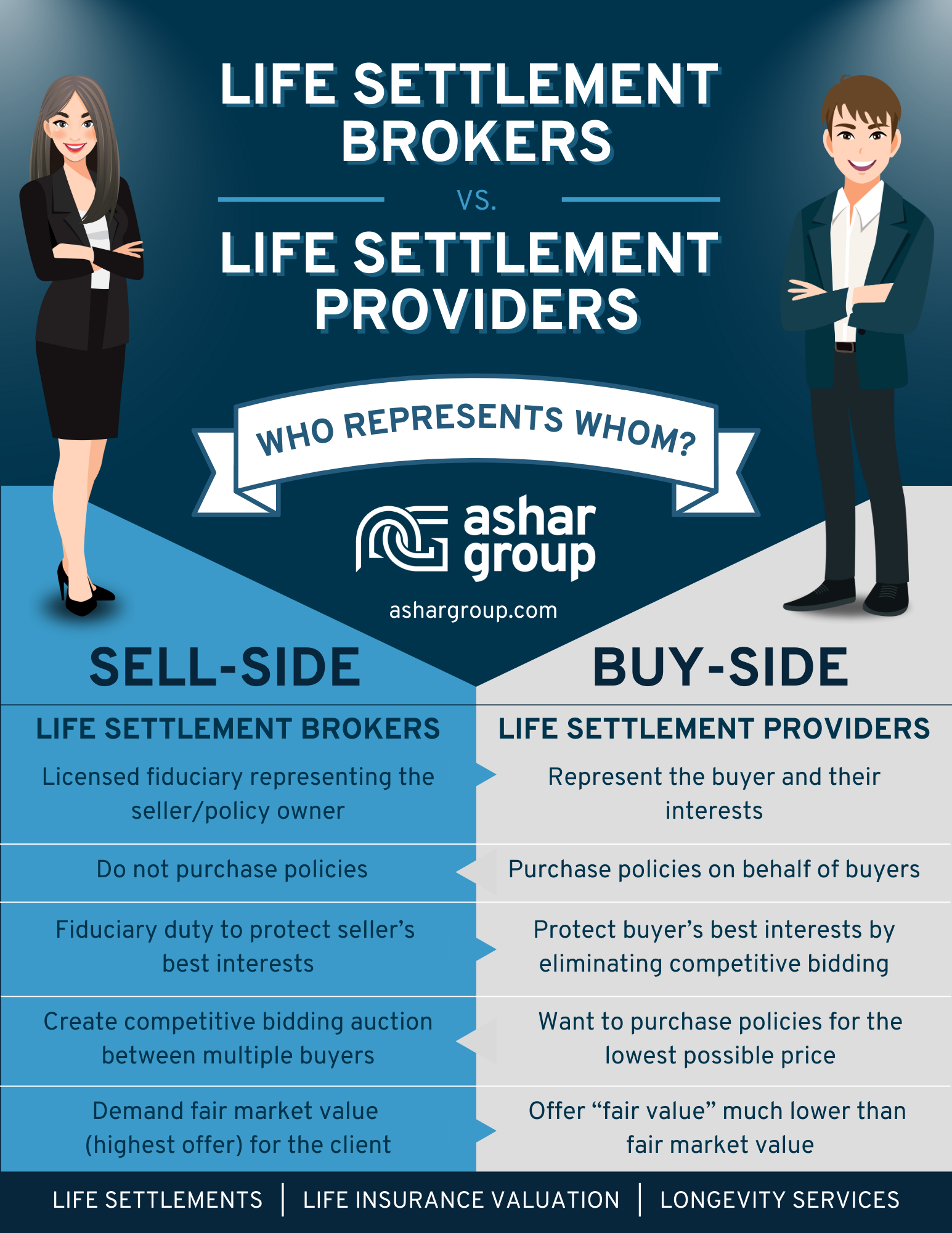

Ashar Group is a nationally licensed independent seller’s representative. We sit on the same side of the table as the planning professional and their client, ensuring the policy owner’s best interests are protected. Because we don’t purchase the policies, our sole responsibility is to the client. Through our auction platform, we create competition between buyers to ensure policy owners are getting the best offer.

PRACTICE TIP: Ask these three questions of your life settlement resource to ensure your client has independent representation in the life settlement transaction:

- Are you licensed to represent the seller or the investor?

- Do you facilitate a transparent policy auction between independent life settlement providers representing multiple institutional funds?

- Does your organization purchase policies, sell life insurance, or manage assets?

Learn more about the difference between sell-side and buy-side.

Ashar Group is a nationally licensed life settlement firm that protects the best interests of policy owners by creating a competitive policy auction to deliver the best value to the seller. Ashar Group does not sell life insurance, manage assets, or purchase policies. We are an independent resource for fiduciary advisors and their clients specializing in life insurance valuation for planning purposes.

{kind=link}