Let’s talk a minute about the benefits of fair market value. Let’s say you owned a nice wooded lot that was considered a valuable piece of real estate. Would you simply forget about it and go about your business as if it never existed? Or give it away for a mere fraction of what you knew it was worth? Of course not. Yet, when it comes to life insurance policies, most people let their policies lapse or surrender without checking to see what they might worth on the secondary market. In fact, more than $90 billion of term policies available on people 65 and older today are being significantly undervalued.

So what determines fair market value of a policy? First, consulting with a Secondary Market Broker can offer the support advisors and their client’s need who are not familiar with the Life Settlement Process. For example, the Ashar Group has something called a SMV®, Secondary Market Valuation. The SMV® generates a variety of competitive bids from many different institutional buyers who are showing interest in the policy. If it is a favorable option for the client, a Secondary Market Broker can help negotiate with providers to determine the fair market value of the policy through this efficient and exhaustive process that takes all factors into consideration. Because of this competitive bidding process, The fair market value can be worth up to 7 times the value of the policy at face value, offering the policy holder a compelling reason to proceed with the Life Settlement process.

If you think it would be prudent for your client to pursue a life settlement, then talk to a secondary market specialist. You can also go to https://ashargroup.com/quiz/ to take the first steps in determining if a policy may qualify for a life settlement. It only takes a minute, and it could help generate the short-term liquidity today that some many people are looking for to help alleviate financial stress in these economic times.

When a client decides to pursue a life settlement arrangement, more often than not it is because an influx of capital is needed to fund a long-term expense like health care. This is why it is very important for the client’s advisor get assistance from a life settlement broker to make sure that multiple bids from different providers are acquired to ensure the most competitive offers. This is key, because multiple bids from the same provider is not achieving fair market value, that’s simply achieving what the provider wants to pay.

A life settlement can provide many times the surrender value to the client when competitively bid right. That’s why it is also important for an advisor to do their research and retain the services of a respected and nationally licensed brokerage firm that has experience and a good industry reputation as a life settlement broker. These secondary market brokers are familiar with the key players and can help get the the best market value for the client.

If you are in a position where you think it would be prudent to consider alternatives, talk to a secondary advisor. You can also go to https://ashargroup.com/policy-value-questionnaire/ to take the first steps in determining if a policy may qualify for a life settlement. It only takes a minute, and it could help save your clients thousands.

For a client considering a Life Settlement, they trust their advisor to serve their best interest. When seeking a life settlement that means a responsibility to obtain the best value for their client with their policy. This is not to be taken lightly, because when clients are looking to a Life Settlement, it is usually due to such factors as paying for mounting health care costs or trying to reduce a large premium that the client can no longer afford and is eating into their retirement savings.

Because of the importance of receiving the highest amount possible, advisors usually turn to a secondary market specialist, who is qualified to find and accept multiple bids to determine the best settlement possible. In turn, due diligence on the part of the secondary market specialist helps protect and enhance the relationship with the client’s advisor. Working together, these advisors now give the client leverage to either sell the policy for an amount much higher than the surrender value or have the option to retain some coverage in the policy with no future payments.

Using a life settlement broker can mean the difference between leverage and litigation: In other words, not checking to uncovering payments significantly exceeding surrender values can lead to lawsuits against the advisor if these options are discovered by another party. Consider this:

- A woman was going to surrender her policy for the $48,000 cash value, because the person handling her trust did not explore the secondary market. Her lawyer however, was familiar with the benefits of the secondary market. In the end, she completed a life settlement and received a lump sum payment of $1,100,000.

With the emergence of the Secondary Market, the potential for a policy to be sold and generate immediate cash flow makes it a serious consideration for advisors who are exploring the best alternative for their clients.

Whatever the reason, prior to the emergence of the Secondary Market, policy owners didn’t have most of these options available to them when surrendering or letting their policy lapse. While traditional exit-strategies are smart choices in some circumstances, the potential for a policy to be sold on the Secondary Market that can generate immediate cash flow makes it an attractive alternative for advisors and their clients.

If you are in a position where you think it would be prudent to consider alternatives, talk to a secondary advisor. You can also go to https://ashargroup.com/policy-value-questionnaire/ to take the first steps in determining if a policy may qualify for a life settlement. It only takes a minute, and it could help save your clients thousands.

There’s no better advocate in helping clients meet their long-term financial goals than their advisor. With this in mind, there are many cases where an uninformed client surrenders or lapses a policy that was worth much more than the cash value. That’s why many advisors choose to order an Ashar Secondary Market Valuation (SMV®) to check for hidden value thereby opening up new options for their client.

For example, a 73 year-old male who was a key executive was retiring from his company. He had a $5,000,000 Term policy that he was going to lapse for $0 that had the option to be converted to a Universal Life policy. The advisor ordered an SMV® and discovered that his client’s policy was worth $1,200,000. This “found money” was included in his retirement package and the company didn’t have to take money out of cash flow for his retirement package. Not a bad way to end a distinguished career and a great reputation enhancer for the advisor.

The point is, by doing your due diligence in analyzing the Secondary Market Value, you have the opportunity enhance a relationship and ensure you’ve done the very best to help your client to fund their lifestyle needs. You can also go tohttps://ashargroup.com/policy-value-questionnaire/ to take the first steps in determining if a policy may qualify for a life settlement. It only takes a minute, and it could help uncover significant value that could be a game changer for your client.

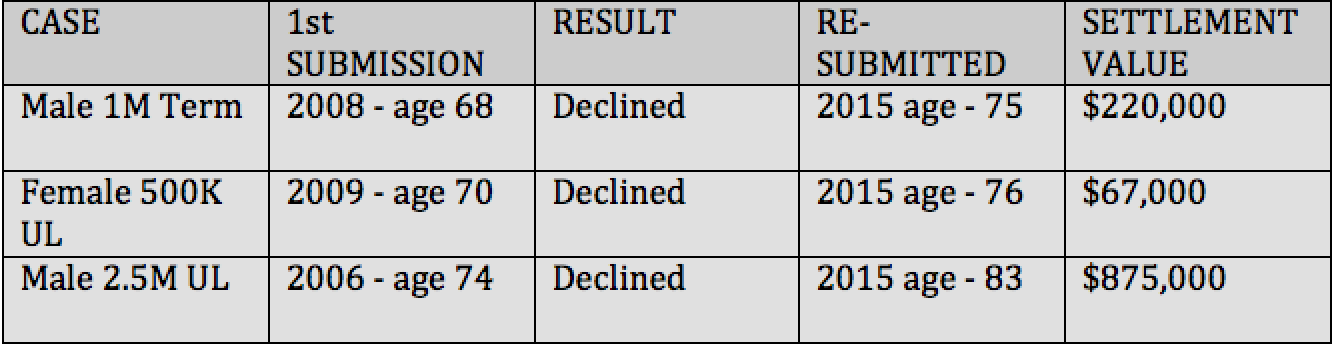

The life settlement market is back stronger than ever and now is a great time to dust off past submissions that didn’t work. Many of the cases closing today were first submitted in the 2004-2008 era. In most situations, its now 10 years later, and not only is the market stronger, but your client is older and may have developed some new health issues.

Give us a call at 800.384.8080 to discuss cases you previously sent to market that didn’t work. We will quickly be able to tell you if your case is a fit for the market today.

How many people are involved in planning the annual fund raising event for most charities? How many man-hours are devoted to just that one single event? There’s a much easier way for charities to raise capital for present needs.

One of the planners we work with asked us to appraise three one million dollar policies that were owned by a charity. The charity was going to surrender them for $50,000. These 3 policies that the charity was about to surrender for $50,000 appraised at more than $800,000! That’s more money than they had raised from their annual fund raising event.

It’s easy to do a quick check for potential present value in a policy owned by a charity. Simply go to https://ashargroup.com/policy-value-questionnaire/ to take the policy value quiz.

Many of your 50 and 60-year-old clients are part of the “Sandwich Generation”. They are striving to prepare for their own retirement and encumbered by the fact that they not only have financial obligations to their children, but many of them are now also faced with caring for a parent who can no longer live independently. You can help your clients caught in this scenario and determine if their elderly parent can qualify for a Long Term Care Life Settlement. That’s a mouthful, but in a nutshell, it means that if their parent is in need of immediate health care to assist in the activities of daily living, they may now qualify for a life settlement that would help pay for their health care expenses. On average, seniors who qualify for a Long Term Care Life Settlement, receive 40-45% of their policy’s face value.

This form of life settlement places the settlement proceeds into a FDIC insured irrevocable benefit trust that is professionally administered with the healthcare payments being made monthly on behalf of the of the individual receiving care. For example: A 77-year-old male was able to sell his $100,000 policy for $45,000. The proceeds were placed in an irrevocable trust and immediately began paying a monthly benefit of $4,500 for 9 months while retaining a funeral benefit of $4500. There are two benefits in this transaction. First, your clients in their 50’s and 60’s now get some relief from having to take funds out of their own investments to pay for mom’s health care. The second benefit is even greater. After months of feeling like a burden to her son, Mom now has the dignity of knowing that she is paying for her own healthcare. That very fact has improved Mom’s quality of life and that’s priceless.

We had one of the families share with us that, “Our mother said that this was the first time in over 10 years that she hasn’t felt like a burden to us.” As you can see, this goes well beyond a monetary gain. Although the adult children were happy to care for their loved one, they now could alleviate the financial strain and tension that this caused between the siblings.

Every year millions of seniors abandon a life insurance policy and get nothing in return for it. According to the Insurance Studies Institute, “90% of seniors who lapsed a life insurance policy would have considered a life settlement had they been aware of the possibility.” If your client is caring for an elderly parent, be sure to explore a life settlement to help pay those costs. This settlement can provide money for home health care, assisted living, nursing home, and hospice care. The gift of dignity when it is needed the most.

If you are wondering whether a policy you own or are entrusted to may be worth more on the secondary market, you can quickly take the first steps by going to https://ashargroup.com/policy-value-questionnaire/. This short quiz can help you in determining if a policy may qualify for a life settlement.

get a secondary opinion®

Life insurance policy owners receive information from the insurance carrier about various policy values such as accumulated value, cash surrender value, guaranteed values, non-guaranteed values, loan value, face amount, and so on. One value that they don’t get from their insurance carrier is fair market value (FMV). For the two most frequently settled life policies, term insurance and universal life insurance with little or no cash value, that FMV can be a life changer for your client. On average, policy owners who sell their polices on the secondary market receive 8 times more value than if they had simply surrendered the policy back to the insurance carrier for cash surrender value. (2010 Government Accountability Office, GAO)

Life insurance policy owners receive information from the insurance carrier about various policy values such as accumulated value, cash surrender value, guaranteed values, non-guaranteed values, loan value, face amount, and so on. One value that they don’t get from their insurance carrier is fair market value (FMV). For the two most frequently settled life policies, term insurance and universal life insurance with little or no cash value, that FMV can be a life changer for your client. On average, policy owners who sell their polices on the secondary market receive 8 times more value than if they had simply surrendered the policy back to the insurance carrier for cash surrender value. (2010 Government Accountability Office, GAO)

Deal or no deal? An offer that represents fair market value is the only deal your client should accept. However, successfully completing a life settlement and obtaining FMV for your client can be a very elusive pursuit if you don’t follow life settlement best practices. It is essential to use an experienced, independent, and unbiased life settlement brokerage firm to design your case and drive value in the auction process. With other players in the life settlement market, such as a provider and/or a buyer, this all important auction process on behalf of your client does not take place. That’s because providers and buyers have a fiduciary duty to the fund they represent, not to your client! It would be a huge mistake for a planner or fiduciary to unknowingly use a provider which would shortchange the client and could potentially lead to a malpractice allegation when it’s discovered that the policy was not put out for competitive bids from multiple institutional buyers.

As a planner or fiduciary it pays to complete your due diligence to make sure you are using a broker that represents you and your client. Here’s what can happen if you don’t: We recently helped a planner who had negotiated a bid for his client of $67,000 from a “settlement firm” that he assumed was getting bids on his clients 1.5 million dollar life insurance policy. Unfortunately, that firm was only trying to get the best deal for their fund. Thankfully, this “Deal” was not consummated. That’s because the advisor attended an insurance conference while this “negotiation” was going on and learned about life settlement best practices and due diligence. Upon returning home he contacted our firm and we took over the case and were able redesign the case and create a competitive auction process that drove the offer up to $248,000 for the same policy that had been offered only $67,000 from a firm that was acting in the capacity of fiduciary to the fund. Without a broker involved, the client would have accepted the $67,000 deal only because it was much greater than the cash surrender value and he didn’t know any better. Use a broker to make sure the deal is a good deal representing fair market value.

For additional information on how to complete your due diligence, please refer to one of our previous articles “Life Settlements: Fiduciaries Demand Fair Market Value and Aren’t Fooled by “Fair Value".

If you think it would be prudent for your client to consider alternatives like the secondary market, talk to a secondary market specialist. You can also go to https://ashargroup.com/policy-value-questionnaire/ to take the first steps in determining if a policy may qualify for a life settlement. It only takes a minute, and it could help save your clients thousands.

Fiduciaries Have to Get it Right!

Life insurance has always been a cornerstone of estate planning and is usually put into place by a knowledgeable life insurance agent. The attorney places the policy in an ILIT and a Trustee is chosen. In the past it was common for the attorney, a CPA, or a Trust Officer to be appointed as a professional trustee of the ILIT.

However, In the mid-90’s, the Uniform Prudent Investor Act (UPIA) changed the landscape for fiduciaries and put the management of life insurance held in an ILIT under the microscope. It was an unwanted intrusion for fiduciaries who where unfamiliar with the constantly changing new breed of life insurance policies used in estate planning beginning with the introduction of Universal Life insurance in the mid-80’s. Innovation didn’t stop there and new life insurance products seem to be introduced all too frequently. It’s challenging for fiduciaries to keep up-to-date on all the policy changes since the advent of the UPIA. Trustees and attorneys have been successful in getting legislation enacted to limit the liability imposed by the UPIA for the management of the life asset held in an ILIT. The liability may be minimized but responsibility to the best interest of the client is still the heart and soul of the fiduciary. Up-to-date knowledge of the secondary life market is needed to get it right.

Fair Market Value - an Essential Tool for Fiduciaries

A whole cottage industry of ILIT Policy Review companies has appeared over the years to take on the responsibility of reviewing ILIT policies and monitoring policy values. There’s only one problem. Most ILIT Policy Reviews do not take into account the analysis of the Fair Market Value (FMV). Being unaware of the FMV could deprive clients from an undetected windfall that could be applied to other parts of the estate plan.

As a result, Ashar Group has developed a Secondary Market Valuation® (SMV) for life insurance to determine FMV. The Ashar SMV® assists attorneys, CPAs, trust officers, fee based advisors, family offices, RIAs, and client centric advisors by providing an accurate formal assessment of life policy fair market value. This willing seller-willing buyer valuation provides an essential data point for sophisticated estate and tax planning.

get a secondary opinion®

Every year a staggering number of senior life policy owners lapse or surrender their unneeded or underperforming life insurance policies without first checking for fair market value. A 1911 Supreme Court Decision, Grigsby v. Russell viewed life insurance as private property whose owner has all of the rights and privileges possessed by other forms of property. The owner has the right to assign or sell the policy. Unfortunately, most senior policy owners are not aware of the benefits of the life settlement market. According to the Insurance Studies Institute, 90% of seniors who lapsed a life insurance policy would have considered a life settlement had they been aware of the possibility.

Think about it:

• Would anybody throw a lottery ticket in the garbage without first checking to see if it had any value?

No! They would check for value first.

• Would you sell your house to a stranger who knocked on your door and offered you more than you thought it was worth?

No! You would get your house appraised to find out if it was worth more.

• Would you abandon your life insurance policy without first checking for fair market value?

Unfortunately, for most people, the answer would be YES! And ………….

when there is a FIDUCIARY involved, then that would definitely be a No No!

Under the right circumstances, uncovering the fair market value of a life insurance policy can be a game changer and provide a significant amount of “found money”.